15 May, 2013

15 May, 2013

A key objective for any open economy is to avoid a financial or balance of payments crisis – a goal that often calls for trade-offs between liberalisation and maintaining control of the economy. This column explores the trade offs India has made.

India increasing openness to the flow of funds in and out of the country presents challenges as well as opportunities. It has left India’s policymakers struggling to strike a balance between key objectives such as nurturing a healthy growth rate, keeping a competitive exchange rate, ensuring moderate inflation and strengthening India’s financial system. This column explores how India has been negotiating theseb rade offs.

A calibrated liberalisation approach

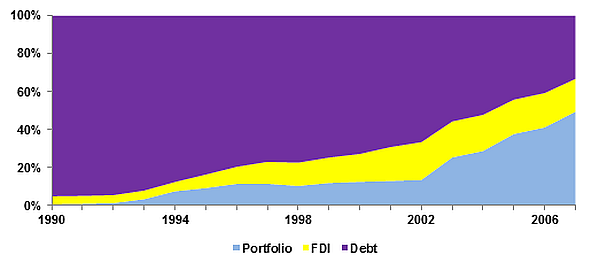

India’s approach to liberalisation of capital controls has been measured. Instead of a ‘big-bang’ opening up of the capital account, India has adopted a gradual approach towards capital account liberalisation, prioritising the liberalisation of non-debt creating flows such as foreign direct investment (FDI) and portfolio flows. These flows involve risk sharing between foreign investors and the host country and thus tend to be more stable than debt flows. While FDI and portfolio flows have been steadily liberalised, debt flows are subject to numerous restrictions. This has resulted in the share of debt liabilities in external liabilities dropping from 95% in 1990 to 33.2% in 2007 (Figure 1). Over the same period the share of portfolio liabilities increased from less than 1% to nearly 50%, while that of FDI went up from 4% to 17.2%.

Notwithstanding the gradual liberalisation, India’s financial integration has steadily gone up since 1991. Gross capital flows have increased nearly 22 times from $42.7 billion in 1991-1992 to over $932.3 billion in 2010-2011. As a share of GDP, this amounted to an increase from 15.5% to 55.2%.

But this calibrated approach has meant that liberalisation of the capital account in India has taken place in fits and starts. And the result has been that India continues to lag behind other major emerging countries such as Brazil, Korea and Russia both in terms of volume of capital flows and regulations governing the flow of capital.

Figure 1. Composition of liabilities in India

Negotiating the trade-offs

A vital objective of calibrated liberalisation of the capital account has been the management of the trade-offs under the so-called macroeconomic ‘trilemma’ – that is, maintaining a stable exchange rate, keeping an open capital account and retaining monetary autonomy. The standard view of the trilemma argues that only two of the three objectives can be achieved at a particular point in time.

To analyse how India has negotiated the trilemma, we quantify the various policy objectives for India under the trilemma (Sen Gupta and Sengupta 2013)), following the method explained in Aizenman et al (2010). We define a variable for each of the three objectives:

- Monetary independence (MI), which depends on the extent to which domestic interest differs from the foreign interest rate.

- Exchange rate stability (ERS), which is calculated by looking at the movement of the Indian rupee compared with other major currencies.

- Capital-account openness index (KO), which is based on net capital flows relative to GDP

Because policymakers can gain greater flexibility with respect to monetary and exchange rate management in the short run by accumulating or running down reserves, we also focus on the change in reserves as a percentage of GDP ( ).

).

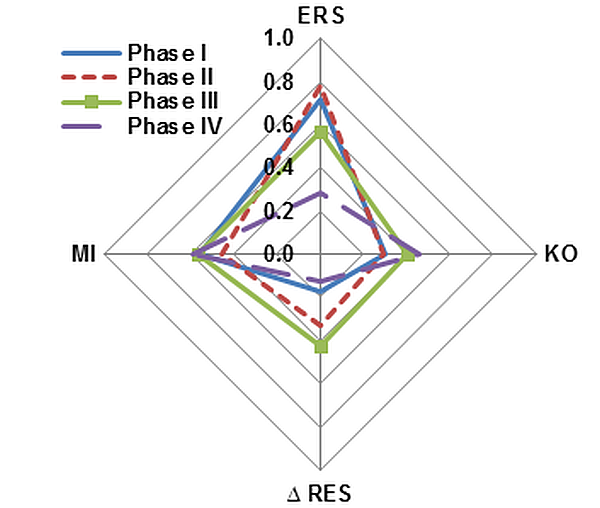

We adjust each variable to between 0 and 1 with 0 indicating closed capital account, completely flexible exchange rate, zero monetary independence and zero reserve accumulation. We divide the entire period into four equal sub-periods (1996-97Q1 to 1999-00Q4, 2000-01Q1 to 2003-04Q4, 2004-05Q1 to 2007-08Q4 and 2008-09Q1 to 2011-12Q3), and plot the average value of the indices in Figure 2.

We find that the rising extent of capital-account openness has been associated with a drop in exchange-rate stability. The index of monetary independence witnessed a drop between 2000-2004 but has recovered in recent years.

Figure 2. Configuration of India’s trilemma objectives and reserves

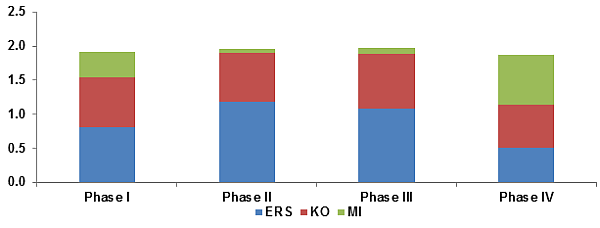

To understand if the trilemma has been binding, we test whether the weighted sum of the three trilemma policy variables adds up to a constant – here set to be 21.

We find that India’s policymakers have opted for the middle ground or an ‘intermediate approach’, juggling the policy objectives as per the demands of the macroeconomic situation. For example, the increase in exchange-rate stability between 2000 and 2008 was associated with a drop in monetary independence. During this period, the Reserve Bank of India (RBI) intervened heavily in the foreign exchange market to prevent the rupee from appreciating in the face of strong capital inflows2. Since 2008, however, India has witnessed a resurgence of monetary independence with a decline in both exchange rate stability and capital account openness3.

Figure 3. Contribution to the trilemma

Reserve Bank of India in the foreign exchange market

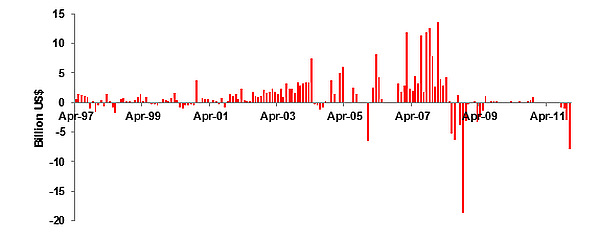

Much of RBI’s intervention in the foreign exchange market has involved accumulating reserves in the face of strong capital inflow to prevent the rupee from appreciating. This has resulted in a steady build-up of reserves since the 2000s with India’s reserve holdings rising manifold between 2001 and 2008 to $315 billion. However, this sustained build-up of reserves contradicts the stated objective of RBI of intervening to iron out the excessive volatility of exchange rate, and not defend any particular value, as that would imply reserve holdings do not change much over a period of time.

Figure 4. Net sale or purchase of US dollar by RBI

The data clearly indicates that the number of months in which RBI purchased reserves were significantly higher than number of months when it sold reserves (Figure 4). This implies the RBI has been intervening in an ‘asymmetric’ manner by buying reserves to prevent the rupee from appreciating but adopting a hands-off approach during periods of depreciation. We test this hypothesis and find evidence supporting asymmetric intervention by the RBI since 1998. Much of the asymmetric intervention took place during 1998 to 2008 when, as a result of resisting appreciation, reserves grew by an average 25% per year. The period following the global financial crisis also witnessed asymmetric intervention despite capital inflows having moderated as the RBI allowed the rupee to depreciate by intervening in a very limited manner.

In a bid to insulate the money supply from the effects of its intervention, the RBI attempted to ‘sterilise’ these interventions. We find that between 1998 and 2004 RBI sterilised nearly 60% of its interventions. Initially the RBI sold government bonds to prevent an increase in money supply. However, by late 2003, the RBI ran out of government bonds and introduced a new mechanism for sterilisation – Market Stabilisation Scheme bonds. The government could not use the proceeds of the sale of these bonds to prevent any impact on the monetary system. The initial ceiling of Rs.0.6 trillion was incrementally increased to Rs.2.5 trillion to counter rising foreign capital inflows. However, a key feature of the scheme lies in the fact that the cost of sterilised intervention became more transparent with the interest payments being reported in the union budget. This kept the scheme bond issuance under check, resulting in the extent of sterilisation dropping to below 30% in the post 2004 period. Thus, between 2004 and 2008, the RBI had allowed the money supply to grow in the face of rising net foreign asset holdings leading to monetary independence being compromised.

Concluding thoughts

There is now an emerging consensus that countries need to actively manage their capital account to protect themselves from the risk of financial crisis and to manage their economies effectively. In a bid to meet these challenges, India’s approach has been one of pragmatism and compromise, adjusting to the changing needs of the economy. One notable trend in recent years has been the shift towards the use of monetary policy. This has been balanced with allowing greater flexibility in the exchange rate, which has acted as a shock absorber during times of volatile capital flows. This approach has suited India well as it has been able to maintain a healthy growth rate, targeted monetary and credit growth rates, moderate inflation rate and a sustainable current account deficit through most of the period. However, in recent months the economy has been facing some challenges on most of these policy fronts largely due to structural bottlenecks and a tepid global economy constraining investment. It will be interesting to see how the policy trade-offs are dealt with in this changing economic scenario.

The views expressed in this article are those of the authors and do not necessarily reflect the views and policies of the Asian Development Bank (ADB) or its Board of Governors or the governments they represent.

Notes:

- According to the trilemma framework, if two of the trilemma policy objectives take the maximum value i.e. 1 then the third objective must take a value of 0.

- Intervention is defined as the official purchase and sale of foreign currencies that a country’s monetary authorities undertake to influence currency movements.

- The outbreak of the subprime crisis in the US led to a flight of foreign capital, which intensified after the collapse of Lehman Brothers. Subsequently, capital flows have remained volatile due to investor uncertainty over the advanced economies’ recovery prospects, large swings in risk aversion, loose monetary policy in the advanced economies and the changing realities in India’s domestic economy. The swings in capital flows were accommodated by allowing the exchange rate to move with greater freedom and through limited intervention in the foreign exchange market. The drop in capital inflows and greater exchange rate flexibility permitted the pursuit of a more independent monetary policy. After the initial softening of monetary policy to stimulate growth, the RBI started tightening the monetary policy from March 2010 in response to high and persistent inflation. This was in contrast with the advanced economies, which were following a soft monetary policy to stimulate growth

- Sterilisation refers to central bank’s insulation of the domestic monetary base from the effect of purchase (sale) of foreign assets by undertaking a corresponding amount of sale (purchase) of domestic bonds.

Further Reading

- Aizenman, J, M Chinn and H Ito (2010), ‘The Emerging Global Financial Architecture: Tracing and Evaluating the New Patterns of the Trilemma Configurations’, Journal of International Money and Finance, 29(4):615-641.

- Hutchison, M, R Sengupta, and N Singh (2011), ‘India’s Trilemma: Financial Liberalization, Exchange Rates and Monetary Policy’, The World Economy, 35(1):3-18.

- Kohli, R (2011), ‘India’s Experience in Navigating the Trilemma: Do Capital Controls Help?’, ICRIER Working Paper 257, June.

- Mohan, R and M Kapur (2009), ‘Managing the Impossible Trinity: Volatile Capital Flows and Indian Monetary Policy’, Stanford Center for International Development Working Paper No. 401

- Obstfeld, M, JC Shambaugh and A Taylor (2010), ‘Financial Stability, the Trilemma, and International Reserves’, American Economic Journal: Macroeconomics, 2(2):57-94.

- Reddy, YV (2008), ‘Management of the Capital Account in India: Some Perspectives’, Reserve Bank of India Bulletin, February.

- Sen Gupta, A and G Manjhi (2012), ‘Negotiating the Trilemma: The Indian Experience’, Global Economy Journal, 12(1):1-20.

- Sen Gupta, A and R Sengupta (2013), ‘Management of Capital Flows in India’, ADB South Asia Working Paper Series No. 17, Manila: Asian Development Bank

Comments will be held for moderation. Your contact information will not be made public.