30 May, 2018

30 May, 2018

In August 2015, the RBI issued in-principle licences to 11 entities to

Even though there are over 157 banks operating in India, a large number of people are not covered by the formal banking system. According to Census 2011, out of 246.7 million households, only 144.8 million have access to banking services. The problem is particularly acute in rural India. Operation costs of running a traditional bank branch in rural areas are very high as sufficient volume of funds is not deposited by the account-holders and loan disbursement is low. For these and other reasons, small-sized banks and foreign banks are usually not interested in opening branches in rural or even semi-rural areas. Hence, it is crucial to think of innovative measures to address the situation. This led to the establishment of payments banks in India.

Evolution of India’s payment system and banking structure

The payment system in India has undergone significant changes since the early 1980s. The Indian banking system has always been a front-runner in adopting modern and latest technology. The Reserve Bank of India (RBI) adopted computerised settlement facilities at all its clearing houses as early as 1988. This was followed by the installation of a core banking software in 2000 and the introduction of internet banking in 2001. In 2007, the Indian Parliament passed the Payment and Settlement Systems Act. Since the inception of this Act, the government has been striving towards a cashless economy. Initiatives taken by the government have created a catalytic environment for the greater proliferation and growth of digital payments. The establishment of the National Payments Corporation of India (NPCI)1 in 2008 and introduction of Real-Time Gross Settlement (RTGS) in 2004, the National Electronic Funds Transfer (NEFT) in 2005, the Immediate Payment Service (IMPS) in 2010, and Unified Payments Interface (UPI) in 2016, are examples of the government’s initiatives in this regard2.

With the aim of restructuring the Indian banking system, the RBI released a discussion paper on ‘Banking Structure in India – The Way Forward’ in August 2013. The paper stressed the importance of empowering the Indian banking sector to cater to the needs of a growing and globalising economy as well as furthering financial inclusion. The paper argued for the need to adopt innovative approaches in banking and to provide access to the formal banking system to low-income households. Subsequent to the release of the paper, in September 2013, the RBI formed an expert committee under the chairmanship of Dr Nachiket Mor to frame a clear and detailed vision for financial inclusion and financial deepening in the country, in addition to several other objectives. The committee submitted its report to the RBI in January 2014, which strongly recommended the licensing of

After incorporating the comments and suggestions given on the draft guidelines, the final guidelines were issued by the RBI in November 2014 to license payments banks.

Out of 41 applications, the RBI issued in-principle licences to 11 applicants to undertake banking business under Section 22(1) of the Banking Regulation Act, 1949. This marked the start of payments banks in India. One of the prime motives behind the establishment of these banks was to provide universal access to banking. Payments banks operate like any other bank, but on a smaller scale. These banks are expected to reach customers mainly through mobile phones rather than traditional bank branches.

At this

Till now, four payments banks have started operations in India. Airtel Payments Bank was the first such bank to start its commercial operation in November 2016 on a pilot basis covering only Rajasthan initially and extending nationwide later in January 2017. Airtel Payments Bank has a network of 250,000 retail stores that also function as banking points. This was followed by India Post Payments Bank (IPPB), which started its branches in Raipur (Chhattisgarh) and Ranchi (Jharkhand) in January 2017, also on a pilot basis. Although the aim was to have

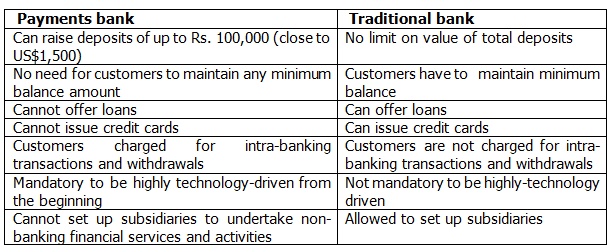

Payments banks vs. traditional banks

While these banks have similarities with traditional banks in terms of functions, there were several differences as well. Some of the major differences are presented in the table below.

Table 1. Differences between payments Bank and traditional bank

A payments bank is different from a mobile banking system. A payment bank is a full-fledged bank, which does not necessarily require a physical branch. It generally uses mobile as

Opportunities and benefits

This is the first time, since its establishment, that the RBI has issued differentiated licences for any banking activity. This RBI initiative is expected to significantly change the banking landscape in India. Indian citizens can experience easier, faster, and hassle-free banking. It is hoped that the absence of a minimum balance requirement would induce more citizens to enter the formal banking system. More and more people from the rural areas and the lower economic strata of the population could be brought under the formal banking system.

The Payments banks have access to the latest technology, a large number of customers, and well-established networks that they can easily leverage in their favour. They also have the opportunity to tap the 233 million people that remain unbanked. As these banks will be operating through their existing business points (for example, Airtel phone stores), their

Challenges and way forward

While there is huge potential, such a banking initiative also faces several challenges. The only medium of operation for these banks is the internet. India is struggling with very low internet speeds – far lower than the global benchmarks. According to Akamai’s State of the Internet report, in the fourth quarter of 2016, the average internet speed in India was 5.6mbps. India’s global rank in this regards is 97, a little behind China and Indonesia, out of the 149 qualifying countries. The low internet speed in the country may hinder the growth of these banks (Shah 2017). Furthermore, since they are entirely technology-based without any significant physical presence, the payments banks appeal chiefly to the tech-savvy citizens. People from the rural areas and small towns in India will find it difficult to participate in this type of banking facility. Efforts should be made to familiarise them with the

Moreover, merely, adding customers or opening accounts

The introduction of payments banks is an important step. However, although India has a modern, technologically advanced banking and payments system, there is still much more effort needed in this sector. It is important to bring more of the rural population under the ambit of

This is a revised version of the manuscript published as Brief No. 565 of Institute of South Asian Studies (ISAS) National University of Singapore on 16 March 2018.

Notes:

- NPCI is an umbrella organisation for operating retail payments and settlement systems in India. It is an initiative of RBI and Indian Banks’ Association (IBA) under the provisions of the Payment and Settlement Systems Act, 2007, for creating a robust payment and Settlement infrastructure in the country.

- RTGS enables fund transfer from one bank to another on a continuous and individual basis (not bunched with any other transaction). Since the

funds settlement takes place in the books of the RBI, the payments are final and irrevocable. NEFT also facilitates one-to-one funds transfer from a bank but the settlement takes place in batches in hourly time slots rather than individually. (Source: https://www.livemint.com/Money/D2HqT88rKHlvl4gryKv6TP/Did-You-Know--The-difference-between-RTGS-and-Neft.html) IMPS facilitates a bank customer to send money electronically immediately to anyone else having an account in any bank. There are no time/day restrictions, as is the case with NEFT. UPI facilitates sending and receiving money using a Virtual Payment Address (VPA) without entering additional bank information. - MDR is the cost charged to a merchant for payment processing services on debit and credit card transactions.

Further Reading

- Reserve Bank of India (2013), ‘Banking structure in India – The way forward’, Discussion Paper, August.

- Reserve Bank of India (2014), ‘Report

of committee on comprehensive financial services for small businessesand low income households ’, January. - Shah, Zahoor Ahmad (2017), “Digital Payment System: Problems and Prospects”, International Journal of Economic and Business Review, Volume 5, Issue 8, August.

By: pallavi 09 July, 2020

This is a very nice one and gives in-depth information. I am really happy with the quality and presentation of the article. I’d really like to appreciate the efforts you get with writing this post. Thanks for sharing. banking classes in pune