08 May, 2023

08 May, 2023

The economic shock caused by the Covid-19 pandemic and longstanding structural issues like the NPA crisis with its associated risk aversion in the banking sector resulted in low bank credit growth in India. Sengupta and Vardhan highlight the trends in and composition of credit growth over the last decade across borrower-classes. They also discuss the emergence and rise of bonds, AIFs, and NBFCs and FinTechs as providers of credit, and the opportunities and regulatory challenges that come with it.

For an emerging economy like India, steady availability of credit for investments is critical for achieving a high GDP growth rate. Historically, the banking system has been the primary formal provider of commercial (that is, non-government) credit. For several years, the Indian banking sector was impaired by a non-performing assets (NPA) crisis. One of the outcomes of this crisis was that, by 2019, total bank credit was growing at 6%, the lowest growth rate in nearly six decades.

In 2020, the Indian economy was hit by the Covid-19 pandemic, which further delayed the revival of bank credit growth. By 2022, the economy had largely recovered from the shock and credit growth bounced back. This triggered widespread optimism that the economy was poised to grow rapidly, supported by a healthy flow of credit. However, this optimism might be misplaced – data released by the RBI shows that there are strong trends of a deceleration of bank credit growth from January 2023 onwards.

Apart from concerns about an impending economic slowdown, this might also reveal longstanding structural issues in the banking system which have persisted through the pandemic. In a recent paper (Sengupta and Vardhan 2023), we highlight some of these trends and the underlying drivers that were conspicuous in India’s credit ecosystem even before the pandemic, and describe the major opportunities and challenges in this space with a way forward.

Pre-pandemic growth and composition of credit

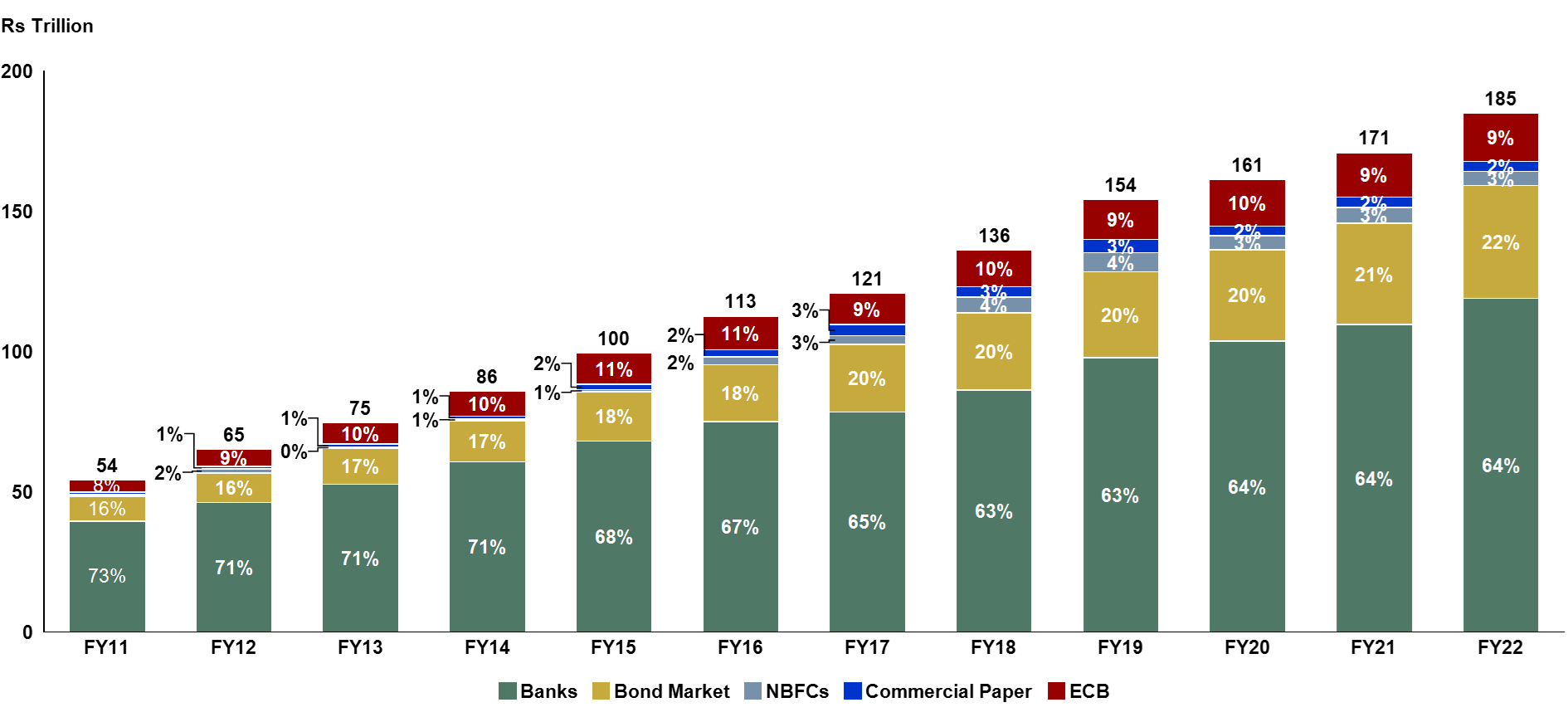

Figure 1 depicts the evolution of the shares of various credit sources over the period from FY2011 to FY2022. Focusing only on the pre-pandemic period, the most noteworthy trend from this figure is that the share of the banking sector as a source of credit declined from 73% in 2011 to 64% in 2020, while the share of the bond market went up from 16% to 20% during the same time. The shares of non-banking financial companies (NBFCs) also inched up.

Figure 1. Shares of various credit sources in total credit, 2011-2022

Source: Authors’ computations using data from RBI, SEBI, and CRISIL.

Notes: i) Financial years are the 12-month periods ending in March of that year. ii) Credit by NBFCs does not include credit from banks and bond market to them.

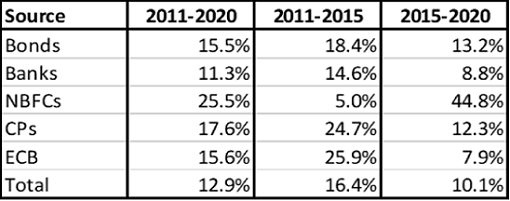

In terms of growth rates, Table 1 shows that over the period between 2011 and 2020, credit from the bond market outpaced that from banks with a compound annual growth rate (CAGR) of 15.5% as against 11.3% for bank credit. A remarkable development was that net credit from NBFCs grew at a staggering rate of 25.5%.

The decadal growth rates, however, obscure the dramatic change that happened during the decade. To throw more light on this, we split the pre-pandemic decade into two halves: 2011-2015 and 2015-2020 (see Table 1).

Table 1. CAGR of commercial credit in India, 2011-2020

Source: Authors’ computations using data from RBI, SEBI, and CRISIL.

Note: CPs are commercial papers, and ECB denotes external commercial borrowing by firms.

We see that, barring NBFCs, there was a sharp decline in growth in the second half of the decade across all other sources of credit. The overall credit growth declined from 16.4% to 10.1%. The only source of credit that experienced a sharp increase in growth rate was the NBFCs, whose credit growth went up from 5% to close to 45%. In contrast, bank credit growth declined from 14.6% to 8.8%.

Despite the decline in the growth rate as well as their share in the credit market, banks still account for nearly two-thirds of total outstanding credit. Within the banking sector, the market shares of public sector banks (PSBs) declined from 77% in 2011 to 60% in 2020, and nearly this entire lost share went to the private banks, whose share went up from 19% to 35%.

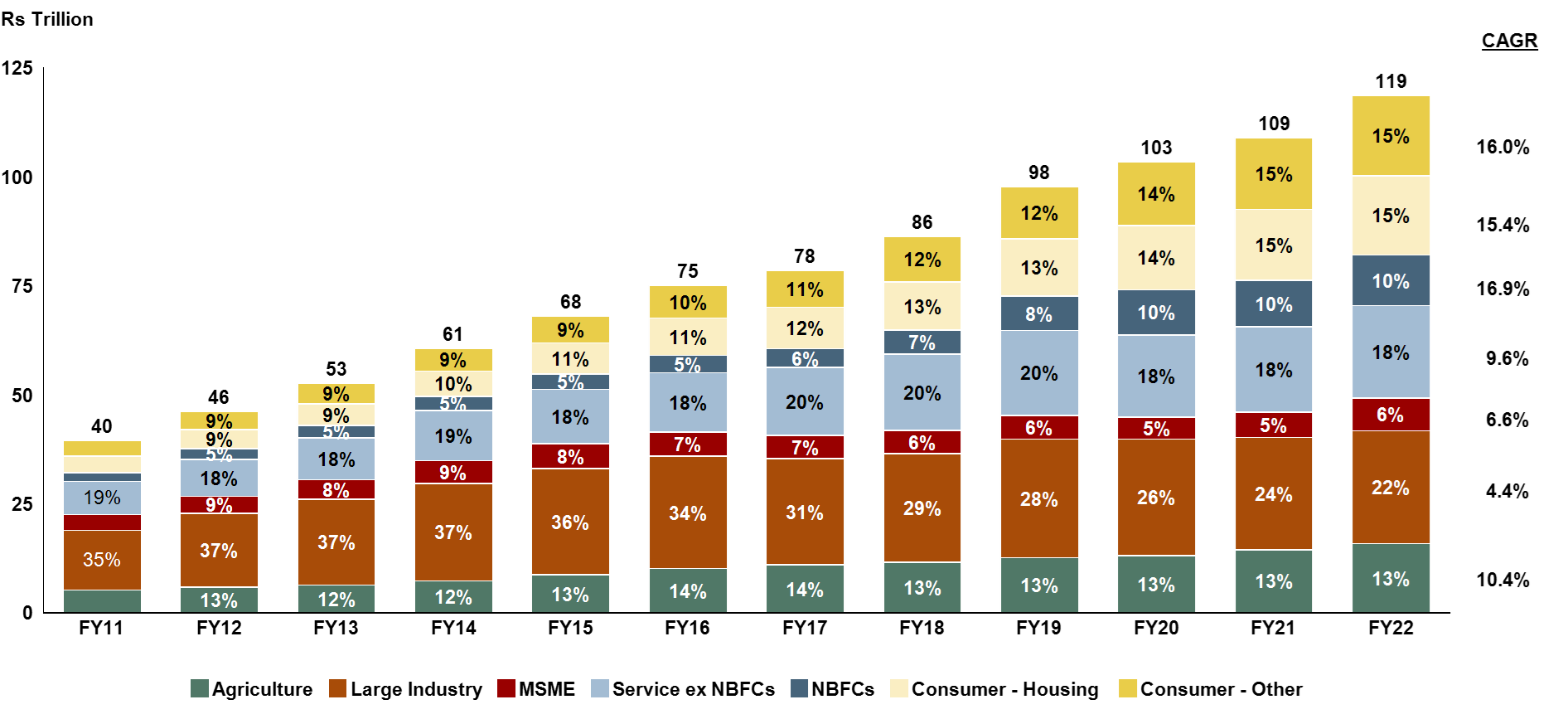

Another noteworthy trend in the pre-pandemic period was a significant ‘consumerisation’ of bank credit. Figure 2 shows that in 2011, the share of industry (large firms and MSMEs) in total bank credit was 44% and it declined to 31% by 2020. On the other hand, the share of consumer credit went up from 19% to 30%. About half of this was unsecured or quasi-secured (secured against weak collateral) consumer credit.

Figure 2. Breakup of bank credit by borrower, 2011-2022

Source: Authors’ computations using RBI data.

Notes: i) Numbers on the stack bars are the shares of the segment in overall credit, and the column of figures to the right are CAGRs of the credit to the corresponding borrower. ii) 'Consumer - Other' indicates unsecured or quasi-secured consumer credit.

Analysing the pre-pandemic trends

The decline in bank credit growth, as well as the fall in the share of industry in total bank credit in the pre-pandemic period, were outcomes of the Twin Balance Sheet (TBS) crisis which manifested in the form of burgeoning NPAs on bank balance sheets, combined with over-leveraged and financially stressed firms in the private corporate sector. The TBS crisis peaked in 2018 when gross NPAs reached almost 12% of total loans. The series of steps taken by the RBI and the government to address the crisis arguably resulted in heightened risk aversion in the banking sector.

With the banking sector struggling, the bond market emerged as an alternative, especially for the top-rated firms. This trend is reflected in the numbers shown in Figure 1 and Table 1. The NBFCs also stepped in – their rise was further aided by the emergence of mutual funds as important players in the financial landscape, yet another notable development during this period.

In 2018, the financial system faced another blow when a large NBFC, the IL&FS (Infrastructure Leasing & Financial Services) defaulted on its debts. This sent shockwaves through the banking system as well as the debt markets – the two biggest funding sources for the NBFC sector. This was followed by other relatively low-impact shocks due to problems in NBFCs such as DHFL (Dewan Housing and Finance Limited) and Indiabulls Housing Finance, as well as in Yes Bank.

Simultaneously, while the NPAs in the banking sector skyrocketed during the period from 2015 to 2020 , the private corporate sector whose financial stress had caused the NPAs to begin with began deleveraging. Leverage of large non-financial firms (measured as the ratio of debt to equity) declined sharply in this period.

The result of heightened risk aversion in the banking system, deleveraging by the non-financial firms, and a series of financial shocks in 2018 and 2019, was that by the time the pandemic hit India, bank credit growth was at an all-time low, the share of retail bank credit had gone up dramatically, and there was a general worsening of risk appetite in the bond markets.

Credit landscape during the pandemic

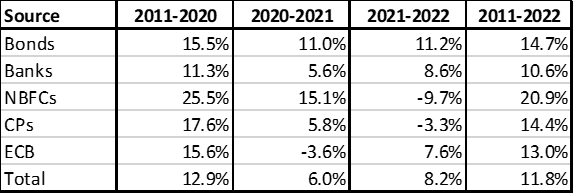

Table 2 shows that during the first year of the pandemic (that is, FY2020-21), credit growth from all sources had slowed down. Bank credit growth had almost halved from 11.3% in the previous decade to 5.6%, although it recovered to 8.6% by FY2021-22. Also drastic was the decline in credit growth from NBFCs, from 25.5% to 15.1% in the first year, followed by a contraction in the next year. Clearly, the pandemic was yet another massive blow to the NBFCs. Bond market credit on the other hand grew at a steady rate of 11% during this period.

Table 2. CAGR of credit across sources, 2011-2022

Source: Authors’ computations using RBI data

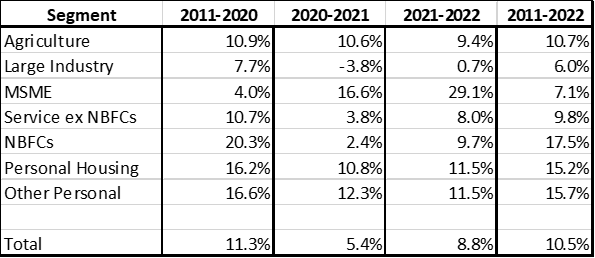

If we focus only on the banking sector and the various borrower classes, we see in Table 3 that while growth of bank credit to agriculture remained steady at 9-10% during the pandemic, credit to large industry shrank and recovered only marginally by FY2021-22. Credit to NBFCs also declined, and average consumer credit growth fell to 10-11% from a CAGR of 16% in the pre-pandemic decade. Though the growth of consumer credit slowed down, it continued to outpace the growth of industrial credit, especially when we take into account credit to the large firms. This shows that the trend of ‘consumerisation’ of bank credit continued during the pandemic.

Table 3. Bank credit growth by segment, 2011-2022

Source: Authors’ computations using RBI data

A notable development was that bank credit to MSMEs grew rapidly, at 16.6% in FY2020-21 and almost by 30% in FY2021-22 compared to the lacklustre growth of 4% in the previous decade. This was primarily driven by the Extended Credit Line Guarantee Scheme (ECLGS) that the government announced in the wake of the pandemic, under which MSMEs could get collateral-free bank loans of up to Rs. 3 trillion with 100% credit guarantee.

By FY2021-22, the banking sector health had improved substantially. This was mostly facilitated by multiple rounds of capital infusion in PSBs by the government, resolution of NPAs by the Insolvency and Bankruptcy Code (IBC), and also the decline in credit growth rate. Gross NPAs fell from 11% of total advances in FY2017-18 to less than 6% in FY2021-22. NPAs for industrial credit declined even more dramatically, from 23% to 8.4%. Undoubtedly this is a significant achievement, considering the stress of the previous decade, the shock of the pandemic and the associated slowdown of the economy. The combination of a healthier banking system and the economy reopening after two years of a pandemic meant that by FY2022-23, bank credit growth witnessed a sharp upturn, averaging at 18%, and bond market issuances also remained strong.

However, it is important to note that the strong revival in credit growth was primarily driven by growth in consumer credit and credit to MSMEs on the back of the ECLGS scheme. Lending to large industries has been stagnant, and there has also been little lending for private sector investment. Over the last one year, bank lending to infrastructure grew by 9%, up from 3% in FY2019-20, but this was fueled mainly by public sector capital expenditure. This is because there are no signs yet of a revival of private investment, which has been sluggish for nearly a decade, and now that the economy has mostly returned to normal after the pandemic, credit growth has begun to taper off amidst concerns of an impending growth slowdown.

The road ahead

The evolution of the credit landscape in India over the last decade or so brings to the fore several opportunities and challenges. The manner in which these will play out will help determine the contours of this landscape over the next decade:

i) Low credit growth: Historically, credit has grown faster than GDP in the Indian economy. The ratio of nominal credit growth to nominal GDP growth for the 60-year period from 1950 to 2020 was about 1.4. However, total commercial credit in India in the decade from 2012 to 2022 grew at a CAGR of 11% - only slightly higher than the nominal GDP CAGR of 10.4%. This implies that the growth of credit in the last decade has been significantly lower than the long-term rate. For India’s GDP to regain a path of high and sustainable growth, it will need a strong revival of private capital investment, for which credit growth will have to be stronger than it has been in the last decade.

In order to achieve this, some of the current impediments to credit supply will have to be removed, including resolving the problem of risk aversion in the banking sector, developing a deeper and more liquid corporate bond market, and encouraging a larger share of foreign debt capital infusion. Each of these areas will require specific policy initiatives.

ii) Rise of the bond market: The last decade saw the share of bonds in overall credit going up from 14% to 22%. The growth rate of credit through bonds also outpaced credit from banks. Slowly and steadily the bond market is becoming an important contributor to the supply of credit in India, especially for the larger, highly rated firms, which is a welcome trend. A less bank-centric financial system would result in better distribution of credit risk in the economy instead of the risk being concentrated in the banking system. The bond market is under the oversight of the Securities and Exchange Board of India (SEBI), implying that with a growing share of the bond market, there will need to be better harmonisation of the regulatory approaches of SEBI and RBI (the banking regulator).

iii) Rise of the credit AIFs: An interesting trend visible in the recent years has been the rise in the bond market investment by credit alternative investment funds (AIFs). This signals the emergence of a private credit market in India. The assets under management of credit AIFs are estimated to be between Rs. 1 and 1.5 trillion. Though they make up only a small percentage of total credit, AIFs are performing an important role because they seek higher returns and hence higher risk, and therefore majority of them invest in bonds that are right above or below the investment grade (that is, bonds ranging from A to B credit rating1). As a result, they are facilitating the development of the lower rated bond market which was non-existent in India until now. High net-worth individuals, family offices, corporate treasuries, as well as foreign portfolio investors are the most common investors in AIFs. Going forward, regulators must encourage the development of these funds in order to deepen the bond market. At the same time, risks arising from this market will need to be better understood, monitored and managed through norms on governance, reporting and disclosures.

iv) NBFCs and FinTechs: The last decade witnessed a dramatic rise in the role of NBFCs as providers of institutional credit in India. In 2022 the RBI, which also regulates NBFCs, changed its regulatory approach – it now has a size-based tiered classification of NBFCs. The largest NBFCs are called the top layer and have far more stringent regulatory oversight compared to the relatively smaller ones. In fact, regulations for the top layer NBFCs are now similar to those for commercial banks. This might diminish some of the intrinsic benefits that the NBFCs introduced to the Indian credit landscape.

In the last few years, technology-led financial firms (or FinTechs) have also seen a phenomenal growth in India. While they have made the greatest impact in the payments space, increasingly FinTechs are entering lending businesses too. It is unclear how these developments will impact the credit landscape in the long run, but in the medium-term we may see NBFC credit growth slowing down. We may also see a large number of partnerships emerging between NBFCs/FinTechs and commercial banks.

v) Consumerisation of credit: As noted earlier, a noteworthy trend in the Indian credit landscape over the last decade was the consistent rise of consumer credit. Of the total consumer credit of about Rs. 60 trillion, about 50% is for housing (secured) and the other half is ‘other’ consumer credit which includes vehicle loans, personal loans, and credit card receivables (quasi-secured or unsecured). The growth of unsecured consumer credit at 20% or more for the last few years increases the likelihood of these borrowers getting into trouble. It is important to note that India does not have a well-defined and modern legal framework to deal with bankruptcy of individuals. This is a segment that the banking regulator will need to monitor with great care.

Conclusion

The pandemic hit the Indian economy at a time when the financial sector, and in particular the banking sector, was dealing with secularly declining credit growth. The pandemic arguably worsened the risk aversion of the financial sector. Two years later, while credit growth has improved to some extent and balance sheets have become healthier, new challenges have cropped up as the Indian economy slows down amidst global headwinds and the structural changes that the financial sector has been undergoing over the last decade.

A consistent reconfiguration of the Indian credit landscape seems underway. From being an overwhelmingly bank-centric system, the supply of credit is steadily getting diversified. Large, high-rated borrowers have migrated to the corporate bond market to source their credit requirements either through bonds or commercial papers. At the lower end of the rating curve, credit AIFs and to some extent NBFCs (including microfinance companies) are becoming dominant. Banks are getting squeezed into the mid rated corporate borrowers (BBB to A rated) and consumer lending.

While this reconfiguration could have a positive outcome of better distribution of risks across savers and investors, it also poses regulatory and policy challenges in terms of ensuring that all segments of the economy have equitable and adequate access to credit and the systemic risk arising from such reconfiguration is contained. In the coming years, these are some of the challenges that the financial sector regulators and policymakers will have to grapple with.

Note:

- Investment grade is a credit rating that signifies that a bond presents a relatively low risk of default. Rating firms use different designations to identify a bond's default probability - "AAA" and "AA" (high credit quality or low default probability) and "A" and "BBB" (medium credit quality) are considered investment grade, while credit ratings below these are considered low credit quality (or high default probability)

Further reading

- Dev, SM and R Sengupta (2022), ‘Covid-19 Pandemic: Impact, Recovery, and the Road Ahead for the Indian Economy,’ Indira Gandhi Institute of Development Research, Mumbai Working Papers 2022-016, Indira Gandhi Institute of Development Research, Mumbai, India.

- Government of India (2017), “The Festering Twin Balance Sheet Problem.” In Economic Survey 2016-17.

- Sengupta, R, LL Son and H Vardhan (2021), ‘A Study of the Non-Banking Finance Companies in India,’ South Asia Working Papers, WPS210381-2, Asian Development Bank.

- Sengupta, R and H Vardhan (2023), ‘India's credit landscape in a post-pandemic world’, forthcoming in I Gupta and M Das (eds.), Contextualizing the COVID pandemic in India: A Development Perspective, Springer.

- Sengupta, R and H Vardhan (2020), ‘The Indian corporate bond market: From the IL&FS default to the pandemic’, The Leap Blog, August 7.

- Sengupta, R and H Vardhan (2019), ‘How banking crisis is impeding India’s economy’, East Asia Forum, October 3.

- Sengupta, Rajeswari and Harsh Vardhan (2017), “This time it is different: Non-performing assets in Indian banks”, Economic & Political Weekly, 52(12)..

Comments will be held for moderation. Your contact information will not be made public.