18 April, 2018

18 April, 2018

While gross expenditure on R&D in India has been on the rise in recent years, it is dominated by public investment. In this post, Sanjib Pohit contends that the current system of allocating public funds for R&D is geared towards low-risk, low-return incremental research, and should instead promote innovative research. He also recommends encouraging private investment in ‘core’ R&D activities via tax incentives.

Economists like Adam Smith had long established a relationship between scientific research and economic growth. Most of the contemporary economists have attributed the sustained growth in developed nations to their intensive research and development (R&D) activities.

If India has to remain relevant in this era of globalisation, it is clear that R&D is critical so that our products remain competitive internationally, and we are able to continuously develop new technologies and products whenever necessary. Furthermore, we need local solutions to deal with myriad local and unique problems that we have. We need to undertake applied research that can focus on areas of national importance like poverty, health and education, to start with.

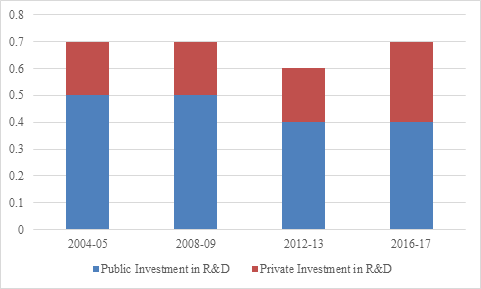

Expenditure on R&D in India

In recent years, gross expenditure on R&D (GERD) has shown a consistently increasing trend from Rs. 18,078 crore in 2004–05 to Rs. 60,869 crore in 2016–17 (Economic Survey, 2017-18, Volume 2). However, as a fraction of GDP (gross domestic product), public expenditure on R&D has been stagnant – between 0.6-0.7% of GDP over the past two decades (see Figure 1). This is significantly below the developed countries/China’s expenditure of about 2% of GDP on R&D with a share of 0.7:1.3 from public and private sector, respectively. Note that India’s R&D expenditure is dominated by public investment. This is in contrast to other countries where private sector is the major player in R&D investment.

Figure 1. Public and private expenditure on R&D expenditure (%)

The biggest bottleneck for public investment in R&D in India is the way funds are allocated. Firstly, most of the public scientific organisations are governed by standard government rules such as auditing, Right to Information, etc. It is generally believed that most of the innovative research would lead to failure. Failure implies that government-nominated committee channelling the funds would be called into question. Hence, committee members would always favour R&D work that focusses on incremental innovation since failure risk is minimal there. It is quite natural for the committee members to be risk-averse since most of them are drawn from government-funded organisations. Besides, the members are only paid honorarium for their work. If path-breaking innovation is expected from public investment in R&D, it is essential to engrain the concept of possible failure in the process.

FDI in R&D

On a positive note, the government has taken a few initiatives to increase involvement of entrepreneurs and researchers, in an attempt to foster scientific innovations. Given the talent pool, several multinational corporations (MNCs) are setting up their R&D centres in India to establish their presence within the country. This will surely encourage R&D and contribute towards a more positive ecosystem for foreign direct investment (FDI). At first glance, increased flow of FDI in R&D seems to be a good sign. However, overall inflows of FDI in R&D mask the nature of these flows. It must be mentioned that not all inflows help enhance the quality of R&D investment and thereby promote innovation and diffusion of new products and technology. The fDi Markets database reports FDI in R&D under three heads namely Design, Development, and Testing (DDT), Education and Training (E&T), and Core R&D. As the name suggests, DDT component of R&D primarily pertains to making foreign products suitable for Indian conditions. On the other hand, the E&T component aims to help diffuse innovative or imported products in the country. The most important component, namely Core R&D, is the one that focusses on making real innovations in the country and may actually help realise the ‘Make in India’ mission.

In India, all these three components are associated with tax benefits. However, this is not case for many of the non-Core R&D activities in other countries, so as to encourage Core R&D activities and generate tax revenues from non-Core ones. For instance, there is long list of activities in Australia that do not benefit from tax exemptions, for example: (a) market research, market testing or market development, and sales promotion (including consumer surveys); (b) management studies or efficiency surveys; (c) maintaining national standards; (d) calibrating secondary standards; (e) activities associated with complying with statutory requirements or standards. Thus, it may be likely that MNCs would consider India as a fertile ground for carrying out many of these activities pertaining to R&D and simultaneously getting tax benefits. It is important to note that Department of Science and Technology (DST) of Government of India – the depositor/collector of R&D statistics in India – has made no attempt so far to collate data according to the three heads mentioned above. Thus, one has no idea about the focus area of R&D expenditure by the domestic public and private sector.

Since the data on FDI in R&D are available by these broad heads in the fDi Markets database, let us examine the priority areas of investment of these R&D centres.

The relevant statistics are collated in Table 1 for the manufacturing sector for the period for which detailed data are available (2007-2011). It can be seen that the average share of Core R&D activities has been about 31% in recent years; DDT activities, which comprise many purely non-Core R&D activities such as sales promotion, constitute a large share. MNCs mainly invest in Core R&D activities in some sub-sectors like biotechnology, chemicals, consumer electronics, medical devices, food and tobacco, engines and turbines, and pharmaceuticals. An in-depth analysis is essential to understand why this trend is exhibited in these sectors. However, sub-sectors like electronic components, textiles, plastics, aerospace, automotive components, automotive Original Equipment Manufacturer (OEM), and minerals mainly attract non-Core R&D activities. The latter are mostly labour-intensive sectors where India has an inherent comparative advantage.

Table 1. Composition of FDI in R&D (%) in manufacturing sector, 2007-2011

| Sub-sector | DDT in total R&D | E&T in total R&D | Core R&D in total R&D |

|---|---|---|---|

| Aerospace | 86.7 | 13.2 | 0.1 |

| Automotive Components | 89.8 | 0 | 10.2 |

| Automotive OEM | 87.5 | 0.9 | 11.6 |

| Beverages | 100 | 0 | 0 |

| Biotechnology | 1.8 | 0.9 | 97.3 |

| Business Machines & Equipment | 84.2 | 0 | 15.8 |

| Chemicals | 40.8 | 2.7 | 56.4 |

| Consumer Electronics | 6.7 | 0 | 93.3 |

| Consumer Products | 82 | 1.1 | 16.9 |

| Electronic Components | 93.6 | 0.9 | 5.5 |

| Engines & Turbines | 64.4 | 4.9 | 30.7 |

| Food & Tobacco | 0 | 4.9 | 95.1 |

| Industrial Machinery, Equipment | 74.6 | 8.9 | 16.5 |

| Medical Devices | 10.2 | 0.5 | 89.3 |

| Metals | 100 | 0 | 0 |

| Minerals | 96.4 | 3.6 | 0 |

| Pharmaceuticals | 9.9 | 0 | 90.1 |

| Plastics | 100 | 0 | 0 |

| Semiconductors | 95.9 | 0 | 4.1 |

| Textiles | 100 | 0 | 0 |

| Average Share | 66.2 | 2.1 | 31.6 |

Source: Computed by author, fDi Markets database

Recommendations

It is clear from the above discussion that India’s tax incentives for R&D expenditure need to be focussed on encouraging Core R&D. Secondly, DST needs to collate R&D data at the disaggregated level. Finally, our system of allocating public funds for R&D expenditure needs to encourage innovative research where potential gains are immense but there is a high probability of failure, rather than incremental research where potential gains are limited although chances of failure are less.

Views are personal.

Further Reading

- Pohit, Sanjib and Pradip Biswas (2016), “FDI in R&D in India: An Introspection”, Turkish Economic Review, 3(3):513-521. Available here.

Comments will be held for moderation. Your contact information will not be made public.