23 July, 2014

23 July, 2014

Various efforts have been made to normalise trade relations between India and Pakistan in the past few years; yet, several barriers remain. This column examines the trade potential in pharmaceuticals – a fast growing sector in world trade – between the two countries. It finds that there is huge, untapped potential in Indo-Pak pharmaceuticals trade, and suggests policy measures to propel trade and investment in the sector.

Trade and investment have been an integral link in improving the relations of South Asia’s two heavy weights, India and Pakistan. With Pakistan’s Prime Minister Nawaz Sharif’s visit to India and Pakistan’s firm commitment to normalising trade ties in the recent times, the prospects of strengthened economic co-operation between India and Pakistan seem bright. From a restrictive trading environment in 2005 when there was no road route, a positive list (a list of items that were allowed to be imported from India) was maintained by Pakistan and the maritime protocol allowed only Indian and Pakistani flagged vessels to carry cargo between the two countries while not permitting the same vessels to carry consignments to a third country (Taneja et al. 2013), trade between the countries has come a long way. The fifth round of talks in April 2011 laid down the blueprint for normalising trade between India and Pakistan (Taneja et al. 2013) and in 2012, Pakistan made a transition from a positive list to a negative list (a list of items that cannot be imported from India). Currently, Pakistan maintains a negative list for India and both countries maintain a sensitive list (a list of products of special interest to individual member countries to which low SAFTA tariffs do not apply) for each other under South Asia Free Trade Area agreement1 (SAFTA).

India granted the MFN (Most Favoured Nation2) status to Pakistan in 1996 and Pakistan is yet to accord the same to India. The asymmetry in grant of the MFN status has been a major stumbling block in improving economic relations between the two countries (John and Bhatnagar 2013). Also, protection of vulnerable sectors3 is what hinders further expansion of India-Pakistan trade.

The pharmaceutical sector is one such segment in which India and Pakistan can integrate, given that it is a fast growing sector in world trade. The global pharmaceutical market has an annual growth rate of 8% and, at that rate, it will cross the value of $1.1 trillion by 2014 (Amir and Zaman 2011). Also, an industry sector like pharmaceuticals, with ‘high social value’ and having direct relation to the health and well-being of consumers, would be an ideal segment to enhance trade and improve relations between the two countries.

Trends in pharmaceutical trade: India and Pakistan

The Indian pharmaceutical industry is the world´s third largest in terms of volume and stands 14th in terms of value. It was estimated at $21.7 billion during 2011 (Kallumal & Bugalaya 2012). As opposed to the Indian pharmaceutical industry, the Pakistan pharmaceutical sector is still at a nascent stage. The industry is the 10th largest in Asia Pacific and was valued at $1.63 billion in 2011 (Amir and Zaman 2011). Another interesting contrast between the industries of both countries is in terms of their export markets: typically, India seems to have a look-west approach (with its major export partners being Europe and US) and Pakistan tends to look more towards the eastern part of the world (its major export partners being South-East Asian countries). In terms of imports, one Asian country that has recently emerged as a common exporter of pharmaceuticals to both India and Pakistan has been China.

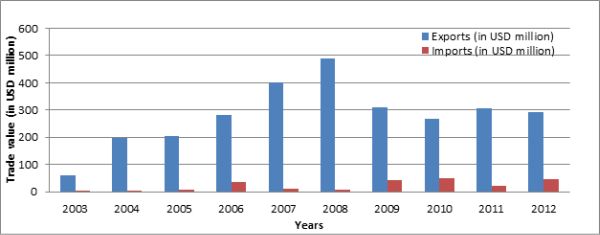

As regards bilateral trade between India and Pakistan, the compound annual growth rate of Indian pharmaceutical exports was 19% over the nine-year period from 2003 to 2012. Data shows that pharmaceutical imports of India from Pakistan have been very small (Figure 1), and command a negligible share (0.002%) in India’s pharmaceutical imports from the world. Indian pharmaceutical exports to Pakistan constitute 1-3% of total Indian pharmaceutical exports. The trade balance in pharmaceutical items has largely been in favour of India, possibly because of the fact that Pakistan’s pharmaceutical sector is still in the developing stage. Since the two countries have common cultures, consumer demand patterns and share a 1,800 km long border, there seems to be some trade potential in pharmaceuticals that can be capitalised on.

Figure 1. Indian pharmaceutical exports to and imports from Pakistan (2003-2012)

Bilateral trade potential in pharmaceuticals

In this context, our research focuses on analysing the inherent trade complementarities in the pharmaceutical sector between the two countries (Pant and Pande 2014). We have followed a basic categorisation of 1) bulk and intermediaries4 , and 2) formulations for pharmaceutical items traded between India and Pakistan.

We use four measures to evaluate the trade potential:

- Trade possibility approach: This looks at items that the two countries can import from each other, instead of importing from elsewhere in the world (Taneja et al. 2013).

- Intra-industry trade (IIT) index: This measures the extent of trade of products belonging to the same industry, between the two countries.

- Trade complementarity index: This measures the extent to which one country’s exports overlap with the other country’s imports (United Nations (UN) and World Trade Organization (WTO) 2012).

- Comparing the regional trade agreements that Pakistan has with India and China: The analysis on the India-China-Pakistan trade dynamics was done in view of China being a major trade partner of both countries and to examine if Indian pharmaceutical items can be substitutes for Chinese exports to Pakistan.

Using data from UN Comtrade, we find that in 2012, there was an untapped trade potential of $1,635.5 million in pharmaceuticals between India and Pakistan. The quantum of export potential ($1,534.6 mn) from India to Pakistan is much more than the import potential ($102.8 mn). In comparison, the actual trade is negligible: Indian pharmaceutical exports to Pakistan in 2012 were about $293.3 million and imports were $47.3 million. The trade complementarity index re-iterates the trade potential in pharmaceuticals between India and Pakistan. The overlap of Pakistan’s export supply with India’s import demand is about 68% whereas, in the case of India’s exports, it is 72%. Hence, there seems to be a fair degree of complementarity between the two countries.

However, the IIT index reveals that this complementarity is not being exploited. The year-wise indices (2009-2012) are rather low, pointing to limited trade in pharmaceuticals between the countries. Another set of indices, the group-wise intra-industry trade indices, reveal that even the limited IIT is occurring mainly in bulk and intermediaries and IIT in formulations, in particular, is almost non-existent5.

Finally, a comparison of Pakistan’s trade agreement with China – the China-Pakistan Free Trade Agreement (CPFTA)6 , and with India (SAFTA) indicates that if open, preferential trading with China has not decimated the Pakistani pharmaceutical industry, there is no reason to expect that liberalising trade with India will do so7.

Perceptions of pharmaceutical industry stakeholders in India and Pakistan

To collect further insights, we conducted interviews with traders, manufacturers and industrialists in the pharmaceutical sectors of both India and Pakistan. There is a general opinion among the stakeholders in Pakistan that liberalising trade with India would lead to an influx of pharmaceutical items which might harm the domestic pharmaceutical industry. The fear of competition is the main reservation of the section of the pharmaceutical industry opposing MFN status to India, apart from other political factors. Many smaller Pakistan pharmaceutical companies have apprehensions regarding the opening up of the sector to India. They also need time to prepare and establish themselves to face competition. However, the Pakistan pharmaceutical sector, due to its “Look East” policy, has been able to compete with the Indian pharmaceutical items in South-Asian markets such as Vietnam and Philippines. Hence, providing market access to India with appropriate trigger mechanisms (like imposing quotas, if necessary) to prevent flooding of Indian pharmaceutical items in the Pakistan pharmaceutical market will facilitate integration of the sectors in the two countries.

However, there are a few big players who are proponents of competition and welcome integration with the Indian pharmaceutical industry. The arguments of the supporters revolve mainly around the following points:

- Gain to the Pakistan pharmaceutical industry from the research and development experience of India

- Direct trade as opposed to indirect trade of bulk and intermediaries that are currently being routed through Dubai

- Larger market access for Pakistan pharmaceutical companies

- Possibility of a better drug regulatory framework with greater exposure to the Indian market

Interviews with Indian exporters of pharmaceuticals to Pakistan brought to light a few ground issues that need attention:

- Weak drug regulatory framework in the Pakistan

- Competitive nature of the Pakistan pharmaceutical market – prices of pharmaceuticals items are quite low

- Logistical issues of banking and visa

- Inclusion of formulations in the negative list as a protectionist measure

Despite the concerns, the outlook of both Pakistani and Indian stakeholders on enhancing trade in pharmaceuticals is very positive and encouraging.

Way forward

Specific to the pharmaceuticals sector, the following policy recommendations are suggested to propel trade and investment:

- To give a push to Indo-Pak trade in pharmaceuticals, it is imperative that the negative list maintained by Pakistan for India should be done away with. Currently, the negative list contains pharmaceutical items of critical importance such as penicillin and its derivatives, erythromicin and its derivatives, ingredients for pesticides, vaccines for veterinary medicine and surgical tapes. In this critical sector, consumer gains should be given greater weightage than temporary production losses.

- Another channel to enhance pharmaceuticals trade would be the removal of raw materials from the sensitive list maintained by Pakistan. The high import duties on raw materials actually reduce the Effective Rate of Protection (ERP) on final products produced in Pakistan. This is because ERP measures the protection given to final goods by subtracting the total tariff paid on imported inputs from the total tariff paid on final products. Hence, the ERP on final goods can be increased by simply reducing the duty on imported inputs.

- Theory recognises that foreign direct investment (FDI) is another way of doing trade, and traversing this path would certainly give a boost to bilateral trade between India and Pakistan. However, the internalisation theory of trade establishes that FDI is the last stage of engagement between countries/companies that trade with each other. So, the prospects of FDI in pharmaceuticals will come later in the future after trade integration between the two countries happens.

- Traditional medicine is a significant area with large potential requiring substantial policy interventions. Herbal, ayurvedic, Sihdha and Unani medicines are common to both India and Pakistan. Although the Government of India has realised Good Manufacturing Practices8 (GMPs) for pharmaceutical manufacturing, the need to establish regulatory mechanisms to regulate herbal medicines is obvious.

- Harmonisation of regulatory regimes is a prerequisite for smooth and uninterrupted trade. The lack of a standardised regulatory framework with respect to manufacturing and the lack of FDA (US Food and Drug Administration) approved laboratories9 in Pakistan have acted as barriers to trade in pharmaceuticals products.

- Lastly, if pharmaceutical trade between India and Pakistan is to expand, it will be necessary to sign mutual recognition agreements (MRAs) that specify standards to be enforced on the drug industry in both countries. Any fears on either side of sub-standard drugs flooding the markets can be addressed via these MRAs.

Notes:

- SAFTA is a trade agreement to promote trade and economic growth in South Asia by reducing tariffs for items that are traded within the region. It was signed in 2004 and came into force in 2006. The members of SAFTA include Nepal, Bhutan, the Maldives, Bangladesh, India, Pakistan and Sri Lanka.

- As members of the World Trade Organization (WTO), countries are supposed to accord "Most Favoured Nation" (MFN) status to each other. MFN is a principle of non-discrimination embodied in the General Agreement on Trade and Tariffs (GATT), which means that countries cannot discriminate between their trading partners.

- Taneja et al. (2013) identifies vulnerable items as those that are most likely to face competition from exports of the competitive partner country. Pakistan considers its automobile and pharmaceutical sectors most susceptible to competition, while India fears competition in the textile sector from Pakistan.

- Bulk and intermediaries are pharmaceutical raw materials used for manufacture of formulations.

- Due to limited data, it is difficult to comment on the trend of the group-wise trade in pharmaceuticals.

- China and Pakistan signed the Free Trade Agreement (FTA) in November 2006 and it took effect from July 2007. It covers the lists for zero-tariff and preferential tariff items along with a tariff reduction modality for other items.

- This had been done by comparing the zero tariff and preferential tariff lists under the CPFTA and the negative and sensitive lists under SAFTA. For more details, see "India-Pakistan Trade: An Analysis of the Pharmaceutical Sector" by the authors.

- Good Manufacturing Practice (GMP) is a system for ensuring that products are consistently produced and controlled according to quality standards. It is designed to minimise the risks involved in any pharmaceutical production that cannot be eliminated through testing the final product (World Health Organization (WHO)).

- Stakeholders in Karachi claimed having only two FDA-approved laboratories for testing in Pakistan – one in Islamabad and another in Karachi.

Further Reading

- Aamir, M and K Zaman (2011), "Review of Pakistan Pharmaceutical Industry: SWOT Analysis", International Journal of Business and Information Technology, p. 114. Retrieved from http://www.rcci.org.pk/wp-content/uploads/2012/12/SWOT.pdf.

- John, W and A Bhatnagar (2013), ‘Nawaz Sharif and India', ORF Issue Brief, Observer Research Foundation, July 2013. http://orfonline.org/cms/export/orfonline/modules/issuebrief/attachments/Issuebrief55_1374051510115.pdf

- Kallummal, M and K Bugalya (2013), ‘Trends in India's Trade in Pharmaceutical Sector: Some Insights', Working paper, Centre for WTO Studies (CWS), Indian Institute of Foreign Trade, New Delhi, 2012. Retrieved from http://wtocentre.iift.ac.in/workingpaper/Working Paper2.pdf.

- Pant, M and D Pande (2014), ‘India-Pakistan Trade: An Analysis of the pharmaceutical sector', ICRIER Working Paper, June 2014. Retrieved from http://icrier.org/pdf/working_paper_275.pdf

- Taneja, N, M Mishita, M Prithvijit, B Samridhi and I Dayal (2013), ‘Normalising India Pakistan Trade', Working Paper, ICRIER, 2013. Retrieved from http://icrier.org/pdf/working_paper_267.pdf.

- United Nations and World Trade Organisation (2012), ‘A Practical Guide to Trade Policy Analysis'. Retrieved from http://www.wto.org/english/res_e/publications_e/wto_unctad12_e.pdf.

Comments will be held for moderation. Your contact information will not be made public.