31 August, 2020

31 August, 2020

While India’s insurance sector has been growing dynamically in recent years, its share in the global insurance market remains abysmally low. This article traces the journey of the Indian insurance sector, and underlines issues such as low penetration and density rates, inadequate investment in insurance products, and the dominant position and deteriorating financial health of public-sector players.

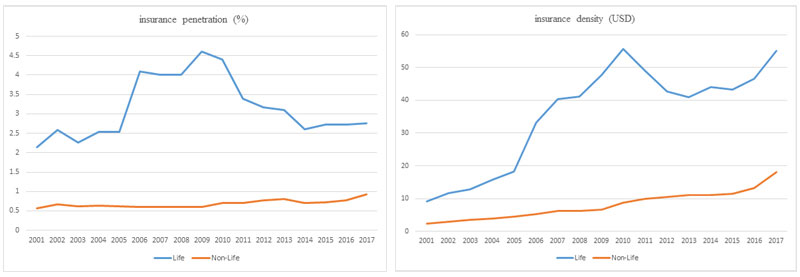

The insurance industry in India has been growing dynamically, with total insurance premiums increasing rapidly, as compared to global counterparts. The insurance penetration (ratio of total premium to GDP (gross domestic product)) and density (ratio of total premium to population) stood at 3.69% and US$ 73, respectively for FY18 (fiscal year 2017-18), which is low in comparison with global levels. These low penetration and density rates reveal the uninsured nature of large sections of population in India, and the presence of an insurance gap. The sector has transitioned from being an exclusive State monopoly to a competitive market, but public-sector insurers hold a greater share of the insurance market even though they are fewer in number. Figure 1 shows the insurance penetration and density in India from 2001 to 2017.

Figure 1. India’s insurance penetration and density: 2001-2017

Source: IRDAI Annual Report, 2018.

The insurance sector has witnessed many changes over the years, including nationalisation of life and non-life sectors (in 1956 and 1972, respectively), constitution of the Insurance Regulatory and Development Authority of India (IRDAI) (in 1999), opening up of the sector to both private and foreign players (in 2000), and increase in the foreign investment cap to 26% from 49% (in 2015). The recent notification of 100% foreign direct investment (FDI) for insurance intermediaries (announced in the Union Budget of 2019-20) has further liberalised the sector.

Further, life insurance dominates the sector with a huge share of 74.7%, with non-life insurance accounting for the remaining 25.3%. In the non-life insurance sector, motor, health, and crop insurance segments are driving growth. India’s non-life insurance penetration is below 1%. In addition, insurance products catering to speciality risks such as catastrophes and cyber security are at a nascent stage of development in the country.

Key challenges facing India’s insurance industry

The insurance sector faces various challenges, as identified and detailed in our recent research (Ray et al. 2020). Low insurance penetration and density rates prevail in India. Rural participation of insurers remains deficient, and life insurers, especially private ones, gravitate towards the urban population, to the detriment of the rural population.

Insurers in India lack sufficient capital, and their financial health, particularly that of the public-sector insurers, is in a precarious state. Among the public-sector general insurers, the financial situation of the ailing National Insurance Company is a cause for concern. Even though the Government of India has already infused Rs. 25 billion in the three public-sector insurers – National Insurance, Oriental Insurance, and United India Insurance – through the first batch of 'supplementary demands for grants'1 for FY20, these insurers require an additional Rs. 100-120 billion in order to meet the stipulated solvency margin.

The general insurance industry recorded a decrease in profits, with public-sector general insurers posting losses, and their private-sector counterparts recording a slight fall in profits in FY19, relative to FY18. While premiums are still growing, the general insurance industry is experiencing underwriting losses, which increased by 45.5% for general insurers in FY19 compared to the previous year (IRDAI, 2019). These might very well be early warning signals of the insurance sector succumbing to the same malaise afflicting banks and NBFCs (non-banking financial companies) in India.

Further, there are concerns in the non-life insurance sector regarding product pricing2 and overcrowding in some segments,3 along with issues in the crop insurance segment.4 To maintain profitability, insurance companies are becoming increasingly dependent on their investment portfolio. They have also resorted to harmful practices, for example, undercutting premiums. Other challenges, such as the predominance of traditional distribution channels,5 also hinder the sector’s growth. Besides, insurers in India are capital-starved.6 A possible additional effect of this low level of capital is incipient new risks, and meagre capital makes it difficult for insurers to rise to the challenge of new risks. Risks associated with the Covid-19 pandemic have recently surfaced, creating further challenges for insurers.7

Insurance penetration: Empirical analysis

There is a myriad of linkages between the insurance sector and macroeconomic development. We seek to capture the relationship between insurance and economic growth in India from 1990-91 to 2017-18 through a simple regression exercise, conducted separately for life, non-life, and total insurance penetration. We find a positive and significant relationship between insurance penetration rates (life, non-life, and total) and economic growth in India. Further, we find that liberalisation (increasing of the FDI cap to 49%) positively influenced the life and total insurance penetration rates, while the effect on non-life insurance is negative and insignificant.

Similarly, we test for the effect of the demonetisation episode of 2016, and find a positive and significant impact of demonetisation on insurance (life and total) penetration rates, whereas the impact on non-life insurance is positive but insignificant.

Low insurance penetration and density in the Indian case may, in part, be on account of insufficient capital with insurers. A preliminary empirical assessment shows a positive and significant relationship between insurance penetration and insurers’ equity capital, in the case of life and non-life insurance in India for the period of analysis. For total insurance, the relationship is positive but insignificant. Additionally, we examine whether liberalisation (increase in FDI cap in 2015) of the insurance sector influences the relationship between equity share capital and insurance penetration. In the case of total and non-life insurance, results imply that the positive relationship between penetration and equity share capital for these two segments is stronger in the years after the hike in the FDI cap as compared to earlier years. For life insurance, the effect of liberalisation on the relationship between penetration and equity share capital is positive but insignificant.

Thus, our analysis makes a case for liberalising the FDI cap for the insurance sector, as it provides capital to the insurers, which in turn positively impacts the insurance penetration rate. In addition, the liberalisation of the sector itself reinforces the positive relationship between insurer capital and insurance penetration.

Way forward

In order to increase the penetration rates and density, uninsured rural areas and the urban poor must be brought under the ambit of insurance coverage. Insurance companies in India will have to show long-term commitment to the rural sector as well, and will have to design products which are suitable for rural people. Insurance companies need to think about their distribution mechanism to work effectively in rural markets. The focus of the insurance sector is steadily shifting towards increasing access of low-cost, simple insurance products, including those that can be sold through online channels. Simultaneously, a complementary thrust to spread awareness and improve financial literacy, particularly the concept of insurance, and its importance, can help. In this context, government insurance schemes such as Pradhan Mantri Jan Arogya Yojana, Pradhan Mantri Fasal Bima Yojana, Pradhan Mantri Suraksha Bima Yojana, and Pradhan Mantri Jeevan Jyoti Bima Yojana are notable contributors in expanding insurance coverage among the population.

The merger of the three public sector general insurers, which has now been called off, could have implications for the future of general insurance in India. The issue of low capital levels needs to be addressed, and there is the related aspect of implementation of a risk-based capital framework.8 Prior to that, the precarious state of public-sector general insurers’ finances should be tackled, and the new regime should find the right mix between the growth of the insurance industry and safeguarding policyholders’ interests.

Another area that necessitates regulatory scrutiny is that of application of technology in insurance. An example is the emergence of ‘InsurTech’, designed to make the claim process simpler and more comprehensible. In this context, the Indian insurance market can gain from the right use of technology and innovation, if a comprehensive framework is created for the sector, keeping the associated challenges in mind. Demographic factors, coupled with increasing awareness and financial literacy, are likely to catalyse the growth of the sector. An enhanced regulatory regime that focusses on increasing insurance coverage will also help.

Note:

- Supplementary grants are the additional grants required to meet the expenditure of the government. These are presented and passed by the Parliament before the end of the financial year.

- Since 2007, except for motor third-party insurance, non-life general insurance companies have had a free market approach to pricing. Due to competition, to maintain the market share, and to keep the premiums competitive, companies have resorted to undercutting premiums.

- Rather than exploring other sectors such as home insurance, or home appliances insurance, major private insurers are overcrowding in certain sectors, such as crop and motor insurance.

- The debate in crop insurance is whether public or private insurers are better. Public and private insurers can coexist, and it is necessary.

- New channels, including online and point-of-sales, are being developed but their market share is insignificant. Enhancing distribution channels holds the key to unlocking growth in penetration and density rates in the Indian insurance sector.

- Also, the Reserve Bank of India (RBI) has put a ceiling on banks’ holdings in insurance companies at 30%.

- Lack of data related to patient profiles, morbidity rates, and cost of treatment, which are required to underwrite risk, will have an effect on the premiums for products designed specifically for Covid-19. Insurers may under or over price their products due to this.

- Risk-based capital is a method of computing the minimum capital that is appropriate for a reporting entity to buttress its entire business operations in view of its size as well as risk profile, according to IRDAI (2017).

Further Reading

- Insurance Regulatory and Development Authority of India (2019), ‘Annual Report 2018-19’, 19 November 2019.

- Insurance Regulatory and Development Authority of India (2017), ‘Report of IRDAI Committee on Risk Based Capital (RBC) Approach and Market Consistent Valuation of Liabilities (MCVL) of Indian Insurance Business’, Part II, July 2017.

- Ray, S, V Thakur and K Bandyopadhyay (2020), ‘India’s insurance sector: challenges and opportunities’, Indian Council for Research on International Economic Relations (ICRIER) Working Paper 394, July.

Comments will be held for moderation. Your contact information will not be made public.