03 January, 2022

03 January, 2022

The National Family Benefit Scheme (NFBS) – which provides financial assistance to families in the event of the death of a breadwinner – has been plagued by low budget allocations, restricted coverage, and administrative hurdles. In this post, Jasmin Naur Hafiz examines these and other implementation issues facing the scheme, and advocates for revamping and consolidating this critical component of India’s social security framework.

In 1995, when India launched the National Social Assistance Programme (NSAP)1, a foundation was laid for an important part of the country’s social security system. Over the years, amidst criticisms of low pension amounts, narrow coverage, and forbidding procedures, the NSAP went through a series of critical modifications and revisions (Dreze and Khera 2017). New schemes were added, pension amounts were revised, and guidelines were improved. Today, the NSAP consists of five schemes: the Indira Gandhi National Old Age Pension Scheme (IGNOAPS), Indira Gandhi National Widow Pension Scheme (IGNWPS), Indira Gandhi National Disability Pension Scheme (IGNDPS), National Family Benefit Scheme (NFBS), and Annapurna2.

Among these five schemes, NFBS has received the least attention in both policy discourse and research literature. The scheme was a part of the NSAP since its inception, but has stagnated over the years. In this post, I examine how the NFBS has weakened considerably in the last decade, plagued by problems in scheme design, budget allocations, coverage, and implementation.

The NFBS provides a one-time lumpsum financial assistance of Rs. 20,000 to families in the event of the death of a breadwinner. The eligibility conditions require that the family be on the official list of “below poverty line” (BPL) households, and the lost breadwinner should have been between 18 and 60 years at the time of death. Every case of death of a breadwinner in the family is eligible for financial assistance3.

Reaching the poorest households

As with several other social welfare schemes, BPL targetting has made NFBS inaccessible to many by its very design. For one, the BPL lists tend to be outdated and are rife with exclusion errors. The criteria for identification of BPL families are non-transparent and difficult to verify. The usage of proxy indicators – such as land ownership for identifying families below the poverty line – fail to capture the true extent of poverty and deprivation. There also remains a vast gap between the erstwhile Planning Commission’s poverty estimates, and the number of BPL households identified as being poor using the methods of the Ministry of Rural Development (Mahamallik and Sahu 2011).

Acknowledging these deficiencies, the revised NSAP guidelines of 2014 (Government of India, 2014) state that if an eligible person has been left out of the BPL list, it is the responsibility of the local governments to ensure inclusion of that person and establish their eligibility for NFBS. The onus of proving eligibility has been clearly placed on the local government officials, rather than on the beneficiary. That, however, would require a major change of mindset on the part of functionaries who are used to requesting multiple documents for the simplest applications.

Alternatively, more inclusive methods of identifying eligible families can ensure that social security benefits reach more needy families. One such method is the exclusion approach, used in some states like Jharkhand and Odisha in the context of the National Food Security Act, whereby all households are eligible by default, unless they meet well-defined exclusion criteria indicating that they are ‘privileged’ households. Yet another approach is the method of self-selection, as in the MNREGA (Mahatma Gandhi National Rural Employment Guarantee Act)4.

Declining budget and coverage

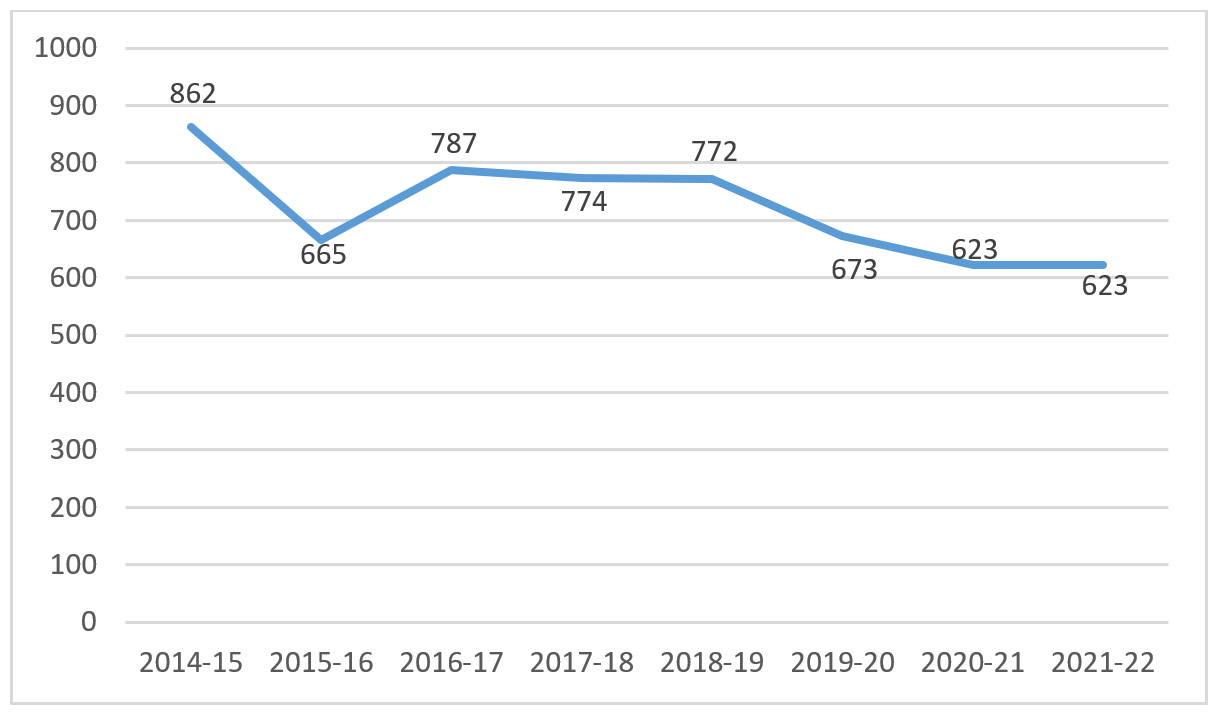

Over the years, the significance of the NFBS in India’s social assistance framework has been consistently falling. One reflection of this is the decline of budgetary allocations for the scheme in the last decade. In 2014, when the NSAP was declared a “core of the core” scheme under the Ministry of Rural Development, the NFBS had a budget allocation of Rs. 862 crores. By 2021-22, this allocation dropped to Rs. 623 crores (Table 1 and Figure 1).

Table 1. Budget estimates, revised estimates, and actual expenditure for NFBS

|

Financial year |

Budget estimates (Rs. crore) |

Revised estimates (Rs. crore) |

Actual expenditure (Rs. crore) |

|

2014-15 |

862 |

N/A |

N/A |

|

2015-16 |

665 |

N/A |

639 |

|

2016-17 |

787 |

787 |

623 |

|

2017-18 |

774 |

708 |

530 |

|

2018-19 |

772 |

675 |

607 |

|

2019-20 |

673 |

622 |

481 |

|

2020-21 |

623 |

481 |

N/A |

|

2021-22 |

623 |

N/A |

N/A |

Source: Annual Union Budget documents (allocation for the Department of Rural Development).

Note: In the absence of scheme-wise allocations for NSAP in the Budget documents of 2014-15 and 2015-16, the NFBS budget figures for these years had to be inferred from the Detailed Demand for Grant.

Figure 1. Budget estimates for NFBS, 2014-15 to 2021-22

Note: All figures are in crore rupees.

The financial stagnation of the scheme is more visible when we look at the revised estimates and actuals. In 2019-20, in spite of a budget estimate of Rs. 673 crore, the actuals were only Rs. 481 crore. The revised estimates for 2020-21 was also reduced to Rs. 481 crore from the budget estimate of Rs. 623 crore.

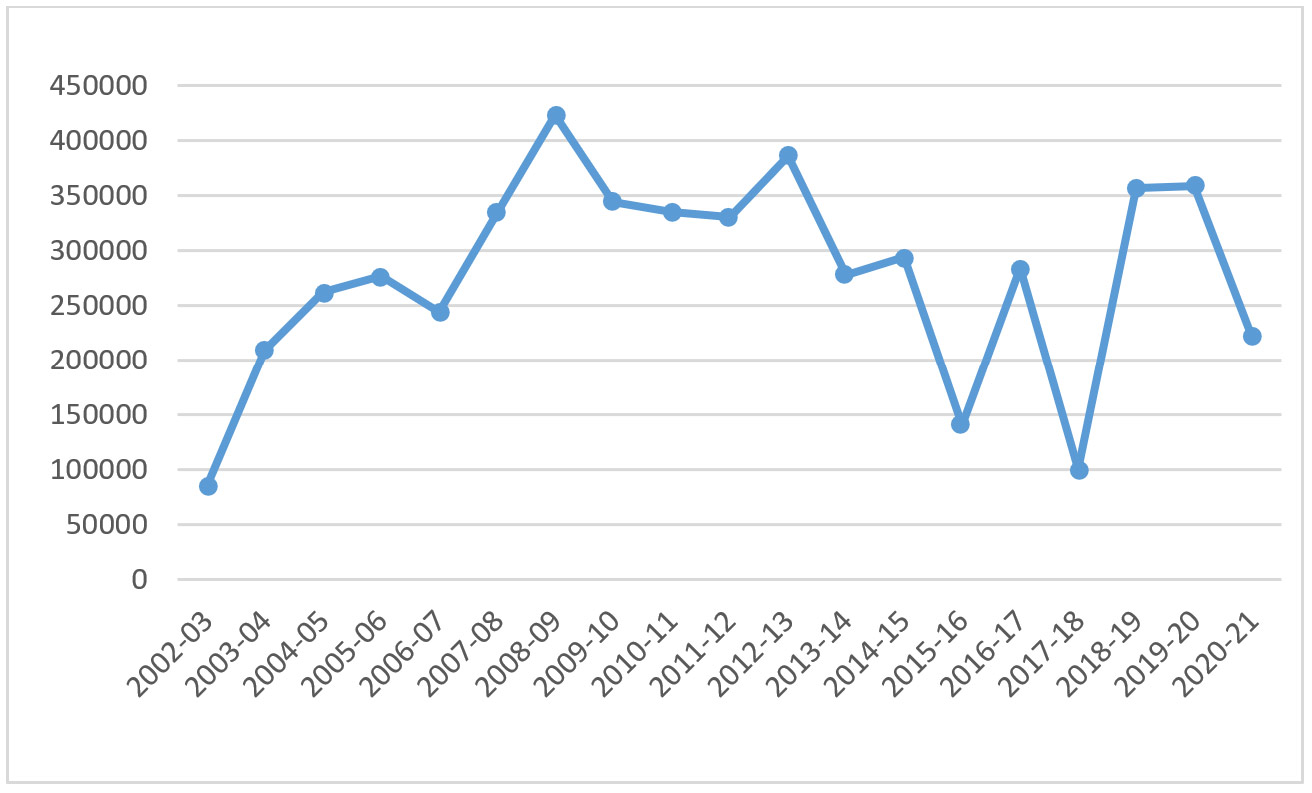

The coverage of NFBS is much lower than that of other NSAP schemes (Table 2). Coverage increased steadily until 2008-09, when it reached a peak of 4.2 lakh beneficiaries, and then hovered around 3 lakh beneficiaries in most years (Figure 2). From 2013-14 onwards, however, there were sharp declines in some years (for example, 2015-16 and 2017-18), and coverage was just 2.2 lakh beneficiaries in 2020-21, the latest year for which data are available.

Table 2. Coverage of beneficiaries under NSAP Schemes (in lakhs)

|

2012-13 |

2013-14 |

2014-15 |

2015-16 |

2016-17 |

|

|

IGNOAPS |

227 |

222 |

221 |

201 |

214 |

|

IGNWPS |

49.7 |

62 |

63.3 |

53.9 |

57.3 |

|

IGNDPS |

10.6 |

10.6 |

10.6 |

6.5 |

7 |

|

Annapurna |

8.4 |

7.8 |

8 |

7.9 |

2.6 |

|

NFBS |

3.6 |

2.8 |

2.9 |

3.6 |

3.6 |

Source: 2020-21 Report of the Standing Committee on Rural Development, Ministry of Rural Development.

Figure 2. Coverage of NFBS, 2002-03 to 2021-22

Sources: Open Government Data Portal, Ministry of Rural Development Annual Reports, NSAP Dashboard.

Notes: (i) In the absence of a single time series spanning from 2002-03 to 2020-21, the data had to be compiled from three different government sources (the open government data portal, NSAP dashboard of the Ministry of Rural Development, and Ministry of Rural Development annual reports). (ii) For some years, there are discrepancies between these three sources. For such years, the graph uses whichever figures are closer to the trend.

Following the recommendations of a 2013 taskforce on NSAP, the eligibility criteria of NFBS were expanded in 2014 to include the death of women who are homemakers in BPL families. Earlier, the term “primary breadwinner” was interpreted as referring to male members of a family. Recognising the discriminatory undertones of such a definition, the eligibility conditions were relaxed to include the death of any adult family member.

The expansion of eligibility criteria in 2014 was expected to raise the number of beneficiaries to 9 lakh a year, with an additional financial outlay of Rs. 900 crore per annum (Government of India, 2013). However, there has been no sustained increase in the coverage of NFBS since 2014 (Figure 2). Furthermore, while these expanded eligibility conditions have been officially recognised in the new NSAP guidelines, there is no corresponding financial commitment in terms of increased budget allocation. In fact, we observe a steady fall in the NFBS budget since 2014 (Table 1). Hence, the guidelines are yet to be applied in practice.

Implementation issues

Earlier this year, the parliamentary standing committee on rural development, in its report to the Lok Sabha (lower house of parliament), severely censured the government for its apparent “laxity” in raising the amount of social security benefits under the NSAP. In 2012, the amount of financial assistance under the NFBS was revised from Rs. 10,000 to Rs. 20,000. However, even the revised amount is grossly inadequate for the dignified survival of a poor family that has lost its breadwinner. These low amounts defeat the very purpose of the scheme.

The scheme is also undermined by complex application processes, and having to prove eligibility is often a huge burden for applicants. One major hurdle for many beneficiaries is the delay involved in obtaining a death certificate for the deceased family member (Nayak 2018). This problem is particularly serious when death occurs in a distant location. For families of migrant workers who have died outside their state, procuring a death certificate is a major impediment in accessing NFBS benefits.

In a 2018 survey of NFBS beneficiaries in Andhra Pradesh’s Chittoor district, it was found that certain Dalit5 households were disqualified on the ground that the age of the deceased breadwinner was more than 25 years at the time of death (Raghupathi 2018). This, however, has no basis in the guidelines, which require the deceased to be between 18 and 60 years of age at the time of death.

Infringement of guidelines by officials becomes easier when public information on the scheme is not easily available to potential applicants. A study of NSAP schemes in Murshidabad district in the state of West Bengal found that gram panchayat officials, public institutions and public libraries could not contribute much to the dissemination of information about the scheme (Mollah 2021). On the other hand, elected representatives, friends, relatives, neighbours, and photocopy centres were found to be the primary networks through which the public accessed information on the scheme. The inadequacy of formal government institutions in providing reliable information excludes many poor families from accessing the benefits of NFBS. Further, the study also found that as the distance from the residence of the respondent to the block development office or the gram panchayat office increases, the likelihood of accessing information and the benefits of the scheme decrease significantly.

Incidents of beneficiaries being paid a wrong amount are not uncommon. Some beneficiaries reported being paid the old amount of Rs. 10,000 instead of the revised amount of Rs. 20,000, that came into effect in 2012 (Raghupathi 2018). Corrupt gram panchayat and post office officials often demand an inducement, resulting in many beneficiaries receiving less than their due. Cases of beneficiaries being pressured to pay “’speed money” to the block authority to ease the application process have also been reported (Nayak 2018).

Corruption also manifests itself in the form of elected representatives and panchayat officials favouring their kith and kin for inclusion in the scheme. The probability of getting benefits from NSAP schemes was found to be three times higher for relatives of officials and elected representatives, relative to others (Mollah 2021).

Implementation hurdles also include frequent delays in NFBS payments. While the official guidelines require benefits to be sanctioned within 60 days of application, there have been reports of NFBS beneficiaries being faced with to massive delays, sometimes running up to three years. Such long delays, once again, defeat the purpose of the scheme.

Modes of payment

Since 2014, which is when the NSAP was officially declared a direct benefit transfer (DBT) scheme, states have been directed to adopt bank accounts as the preferred mode of payment. Cash transactions are actively discouraged in a bid to reduce leakages. The revised NSAP guidelines of 2014, however, mention that the guiding principle in choosing the mode of payment must be the convenience of the beneficiary. If it is found that the beneficiaries have to make a cumbersome journey to access their bank accounts, the guidelines require that doorstep payments be arranged. If the beneficiary is infirm or old, it has to be ensured that the beneficiary does not have to travel more than three kilometres to access their pension account.

However, in reality, these guidelines are not followed. Very often, beneficiaries have to bear high collection costs due to the long distances that they have to travel to access their bank account. This sometimes requires multiple trips to the bank and long waiting hours, thereby proving inconvenient for beneficiaries. The practice of the Aadhaar6 seeding of bank accounts has possibly created further issues, judging from the experience of similar schemes such as the maternity benefit scheme (Drèze et al. 2021).

The payment modalities are, however, state-specific. Some states, like Odisha, continue to rely heavily on cash payments for NFBS. The Odisha government presents a good example of developing a payment system for social security benefits that is convenient for the recipients. Besides NSAP schemes, Odisha has its own social security benefit scheme called the Madhu Babu Pension Scheme (MBPS). Through this scheme, regular cash payments are made through the gram panchayat office on a fixed day of the month. This has been shown to ensure community participation and greater accountability (Chopra and Pudussery-2014). The Odisha example also indicates that technology-enabled payment systems with biometric verification are not necessarily required to reduce leakages and improve payment efficiency. A traditional cash-based payment system, when implemented with regularity and people’s participation also serves the purpose (Chopra and Pudussery 2014).

These payment issues are perhaps less critical for the NFBS than for other NSAP schemes, since the NFBS involves a one-off payment rather than a monthly pension. Yet, a reliable and timely payment system is essential for any social assistance scheme.

The way forward

In 2014, the NSAP taskforce presented a list of recommendations to the central government that could potentially revamp the scheme and make it more people-friendly (Government of India, 2013). One of these was to raise the amount of benefits paid under NFBS. K.P. Kannan, a member of the taskforce, observed that when the government set this amount at Rs. 10,000 in 1995, the method used was to provide an amount equivalent to 80% of India’s then per capita GDP (gross domestic product). Based on that method, he pointed out, that NFBS benefits should have risen to Rs. 60,000 by 2014, instead of the prevailing Rs. 20,000.

Harsh Mander, another member, recommended that the amount of assistance be raised to around Rs. 25,000, so as to be equivalent to around six months of minimum wages for one person. The value of the original amount of Rs. 10,000 was found to be Rs. 29,544 in 2014 using the CPI (consumer price index)-Industrial Workers Index. The committee recommended that the amount of benefits be indexed to the price level, employing the method used to pay dearness allowances to central government employees.

The committee also recommended the replacement of the BPL targetting methodology with the exclusion approach, using exclusion criteria based on the Socio-Economic and Caste Census of 2011. Expanding coverage to provide the benefits of NSAP to all families eligible for food rations under the National Food Security Act by 2016-17, along with other recommendations to ease difficulties in collection of benefits have also been proposed.

While these recommendations are a step in the right direction, ensuring that they materialise at the ground level continues to remain a challenge. Stronger financial commitment and political will are key to revamping NSAP schemes, including NFBS, and consolidating this critical component of India’s social security framework.

I4I is on Telegram. Please click here (@Ideas4India) to subscribe to our channel for quick updates on our content

Notes:

- The National Social Assistance Programme is a centrally sponsored scheme providing financial assistance in the form of social pensions, to the elderly, widows, and persons with disabilities.

- The Annapurna Scheme aims at providing food security to meet the requirements of those senior citizens who though eligible, have remained uncovered under the National Old Age Pension Scheme (NOAPS). Under the Annapurna Scheme, 10 kilograms of foodgrains per month are to be provided free of cost to the beneficiary.

- The responsibility of identifying eligible beneficiaries, rests primarily with the gram panchayats and municipalities. The available BPL list of each state is to be taken as the primary document for establishing eligibility. A gram panchayat is the cornerstone of a local self-government organisation in India of the Panchayati Raj system at the village or small-town level and has a sarpanch as its elected head.

- MNREGA offers a guarantee of 100 days of wage-employment in a year to a rural household whose adult members are willing to do unskilled manual work at the prescribed minimum wage.

- According to the Indian caste system, Dalits (officially Scheduled Castes) are members of the lowest castes who have been subjected to the practice of untouchability.

- Aadhaar or Unique Identification (UID) number is a 12-digit identification number linked to an individual’s biometrics (fingerprints, iris, and photographs), issued to Indian residents by the Unique Identification Authority of India (UIDAI) on behalf of the Government of India.

Further Reading

- Chopra, Saloni and Jessica Pudussery (2014), “Social Security Pensions in India: An Assessment”, Economic and Political Weekly, 49(19): 68-74.

- Drèze, Jean and Reetika Khera (2017), “Recent Social Security Initiatives in India”, World Development, 98: 555-572.

- Drèze, Jean, Reetika Khera and Anmol Somanchi (2021), “Maternity Entitlements in India: Women's Rights Derailed”, Economic and Political Weekly, forthcoming.

- Mahamallik, Motilal and Gagan Bihari Sahu (2011), “Identification of the Poor: Errors of Exclusion and Inclusion”, Economic and Political Weekly, 46(9): 71-77.

- Government of India (2013), ‘Proposal for Comprehensive National Social Assistance Programme: Report of the Task Force’, Ministry of Rural Development.

- Government of India (2014), ‘National Social Assistance Programme: Programme Guidelines’, Ministry of Rural Development.Mollah, Niti (2021), “The Role of Information in Availing the Benefits of NSAP Schemes: A Study of Murshidabad District, West Bengal”, Library Philosophy and Practice (e-journal), 5162. Available here.

- Nayak, A (2018), ‘Population ageing in West Bengal with special reference to social security’, Doctoral dissertation, University of North Bengal. Available here.

- Raghupati, P (2018), “National Social Assistance (NSA) Programme: A Study on Women Beneficiaries among Dalits and Non-Dalits”, Journal of Economics Policy and Research, 13(2): 68-80.

Comments will be held for moderation. Your contact information will not be made public.