23 March, 2017

23 March, 2017

Firms in India often find it difficult to purchase land, resulting in projects being delayed, relocated, or cancelled. Analysing firm- and state-level data, this column explores the impact of post-independence land reforms – especially those related to land ceilings - on corporate investment in the country.

As India strives to grow through liberalisation and industrialisation, firms find it difficult to purchase land; this often leads to tussles between farmers, industrialists and government. While the reasons behind this difficulty are unclear, anecdotal evidence suggests that the consequences are both visible and sizeable: Projects are delayed, relocated, or cancelled1.

In this column, we shed light on some of the causes and consequences of firms’ difficulty to purchase land. Specifically, we ask whether the historical land reforms that followed India’s independence, especially those related to land ceilings, make it more difficult to purchase land, and whether these difficulties have an effect on corporate investment (Pal and Saher 2017).

Land ceiling legislations and corporate investment

While India’s land reform programme had various components, our analysis, particularly focusses on the role of land ceiling legislations defining the ceiling size of land holdings. By 1961-62, ceiling legislations were passed in all states. The size of the ceiling varied from state to state, and was different for food and cash crops. The unit of application of ceiling also differed across states: in some states ceilings were based on ´land holder´, whereas in others ceilings were based on ´family´. In order to bring about uniformity and comparability, a new policy was introduced in 1971 based on the fertility of the land. Different land ceilings were imposed on three categories of land: land cultivated with two crops, land cultivated with one crop, and dry land. The size of ceilings was the lowest for the land cultivated with two crops.

Our conjecture is that India’s land ceiling legislations ultimately increased the transaction costs of buying land and the price premium firms pay when acquiring land. In reaction to higher land costs, firms find it optimal to invest less in land and capital.

Transaction costs increased after India’s land reforms because, by imposing land ceilings, the reforms redistributed land from a few large landowners to many small owners. A firm looking to acquire a plot of a given size has to negotiate and buy land from a larger number of owners after the reform than before. Each of these acquisitions is costly, and the larger their number, the larger the transaction costs.

Much for the same reason, the price premium that firms pay to acquire land is higher after these land reforms. Once a firm acquires a substantial number of parcels of the plot it wants to buy, the landowners of the remaining parcels, knowing that it is costly for the firm to engage in multiple new transactions for a different plot, may refuse to sell or demand a premium – a rent – above the market price of their land2.

Transaction costs and a price premium disincentivise firms from investing in land. The disincentive extends to capital investments especially when land and capital are complements, such as in the case of the automobile sector (Ghatak et al. 2013), or, when capital cannot easily substitute land.

Empirical evidence

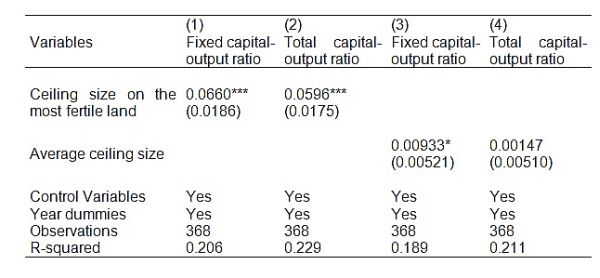

The results from our empirical analysis are supportive of the conjecture that India’s land ceilings lead to less corporate investment. Using a dataset of publicly-traded companies between 1996 and 2012, together with state-level data for 16 major Indian states from 1960 to 1985, we assess the effect of land ceiling size on fixed and total capital-output ratios. In this assessment we control for various observable economic variables, unobservable firm and state-level factors, and also time trends that may influence capital investment. In Table 1, we summarise the state-level results using ceiling size for the most fertile land (columns 1 and 2) and also the average ceiling size (columns 3 and 4) in each state. The average land ceiling is the average of the ceilings for the different types of land weighted by the share of each land type in a given state. The coefficient estimates on the ceiling size on the most fertile land are positive in both column 1 and column 2, which suggest that for each unit increase in ceiling size, fixed (column 1) and total (column 2) capital-output ratios increase significantly. The corresponding effects are not as significant when we consider the average ceiling size (columns 3 and 4). Accordingly, we conclude that controlling for other factors, states with low fertile-land ceilings tend to have lower investment in capital than those with high fertile-land ceilings.

Table 1. Relationship between land ceilings and investment in fixed and total capital-output ratios

Notes: (i) The following are controlled for: Net domestic product, population density, share of population of scheduled castes and tribes, share of urban population, literacy rate, soil fertility, natural logarithm of man days lost due to strikes, and a constant. (ii) Robust standard errors in parentheses. (iii) *** p <0.01; ** p<0.05; * p<0.1. span="">

Notes: (i) The following are controlled for: Net domestic product, population density, share of population of scheduled castes and tribes, share of urban population, literacy rate, soil fertility, natural logarithm of man days lost due to strikes, and a constant. (ii) Robust standard errors in parentheses. (iii) *** p <0.01; ** p<0.05; * p<0.1. span="">

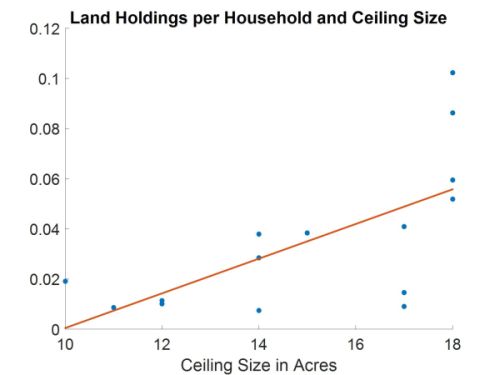

We also find direct evidence supporting the mechanism behind our conjecture. Specifically, we find that the size of household land holdings is smaller in states with more restrictive ceilings. Figure 1 illustrates this point. Smaller land plots suggest more land fragmentation, that is, a larger number of owners per unit of land, and thus higher transaction costs for acquiring a given acreage of land.

While we interpret the evidence in Table 1 and Figure 1 as suggesting that lower land ceilings result in less corporate investment, one could use the same evidence to support the reverse causal relation: states with expectations of low investment set more restrictive ceilings. However, ceiling sizes were not under the control of state governments. By and large, land ceilings were determined by the share of food crops before 1971, and by the quality of the soil from 1971 onwards.

Finally, we rule out a number of competing explanations of our results. Pro-worker regulation in states with more restrictive land ceilings (Besley and Burgess 2002) and higher land prices could also explain the lower corporate investment we observe in those states. To account for these effects, we add two control variables to our regressions: soil fertility – a proxy of land price – and the number of annual man-days lost because of strike activities – a proxy for pro-worker regulation. We find that more restrictive land ceilings still lead to less investment after controlling for these variables. Lastly, we show that the central result holds even after we drop Kerala and West Bengal from the sample - two states where the land reform legislations were implemented most successfully.

Figure 1. Relationship between ceiling size and average household land holdings

Concluding remarks

To conclude, our results highlight an unintended consequence of land ceilings on corporate investment. Ultimately, lower investment leads to lower economic growth. While one cannot reverse the adverse effects of historical land reform, in a land-scarce economy with growing population to feed, options for future policy development require closer scrutiny accounting for the diversity across the states.

Notes:

- Examples include the Tata Nano and Narmada dam projects.

- In the same spirit as our argument, Roy Chowdhury (2013) theoretically argues that, in the absence of politicisation, more fragmentation increases the possibility that landowners refrain from selling their land and demand a premium above the market price of land.

Further Reading

- Besley, Timothy J. and Robin Burgess (2004), “Can labour regulation hinder economic performance? Evidence from India”, Quarterly Journal of Economics, Vol. 119(1):91-134.

- Chakravorty, Sanjoy (2013), “A New Price Regime: Land Markets in Urban and Rural India”, Economic and Political Weekly, Vol. 48, Issue No. 17. Available here.

- Roy Chowdhury, Prabal (2013), “Land Acquisition: Political intervention, fragmentation and voice”, Journal of Economic Behaviour and Organization, 85:63-78.

- Ghatak, M, S Mitra, D Mookherjee and A Nath (2013), ‘Land acquisition and compensation in Singur: what really happened?’, Working Paper, Department of Economics, University of Warwick, CAGE Online Working Paper Series, Volume 2013.

- Mehta, L. (2015), Displaced by Development, Institute of Development Studies, University of Sussex.

- Pal, S and Z Saher (2017), ‘An Unintended Consequence of Historical Land Ceiling Legislations: Impact on Land Acquisition and Corporate Investment in India’, SSRN working paper.

- Singh, G (2016), ‘Land in India: Market price vs. fundamental value’, Ideas for India, 29 February 2016.

- Singh, R (2013), ‘Litigation over Eminent Domain Compensation’, Working paper, International Growth Centre (IGC).

Comments will be held for moderation. Your contact information will not be made public.