24 April, 2013

24 April, 2013

The Indian economy has been facing challenges in the form of sluggish growth, high inflation, and rising fiscal and current account deficits. This column highlights trends in the economic conditions, and outlines policy actions and reforms needed to put the economy back on track.

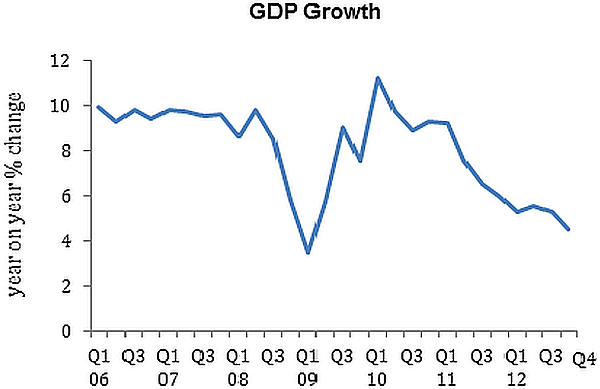

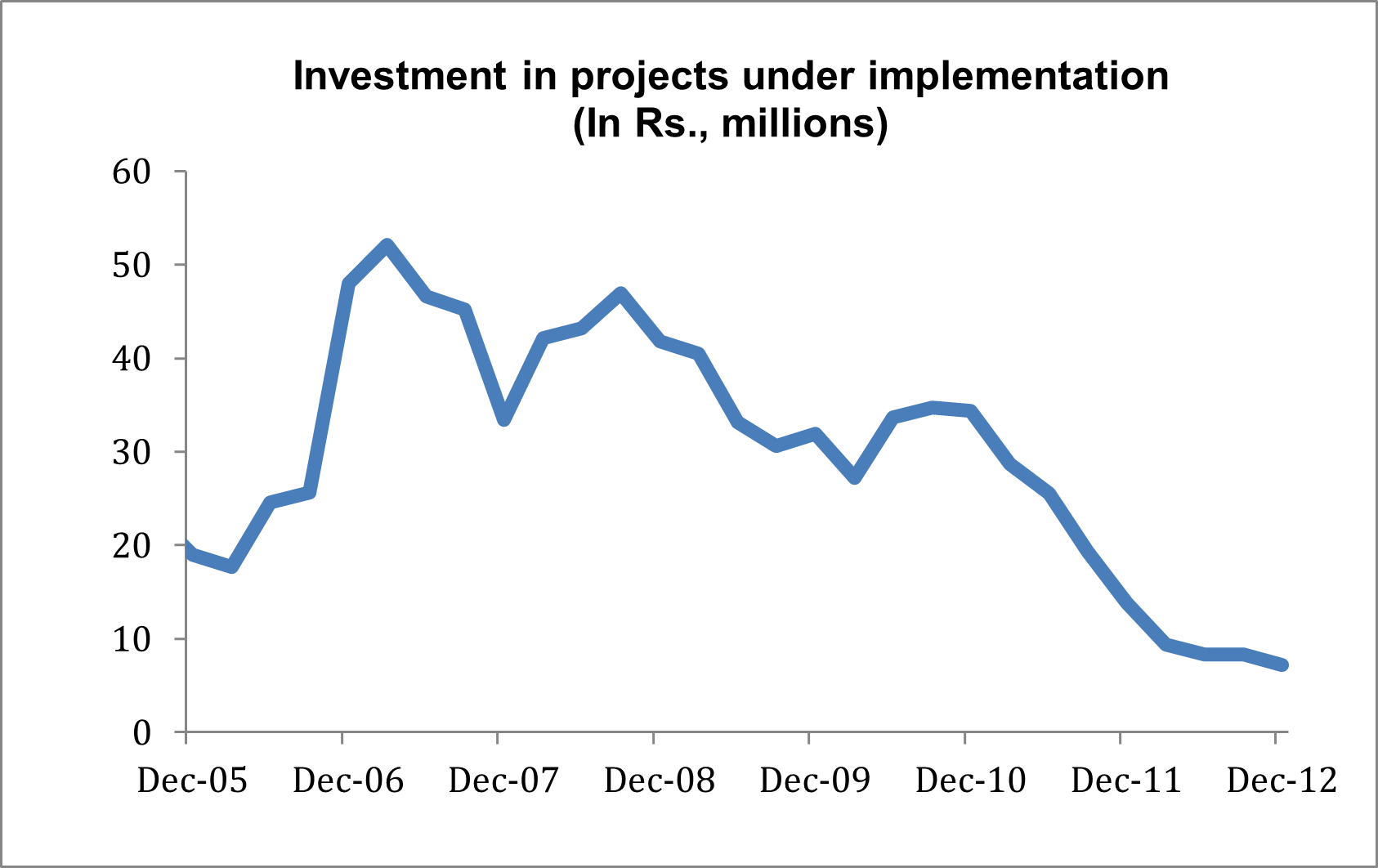

India’s economy faced a challenging 2012. This is reflected by the continued slowing down of GDP growth (Figure 1), inflationary pressures, and persistently high fiscal and current account deficits. The situation is further worsened by the sharp fall in the value of the rupee against the US dollar (25% decline since mid-2011). Besides, there is little sign of improvement in investment. Despite the government embarking on a reform programme in September last year, which included a long-awaited opening up to foreign direct investment (FDI), overall investment activity has remained subdued. Figure 2 shows a sustained slide in investment projects under implementation.

Therefore, whilst the reforms implemented by the government have somewhat assuaged investor sentiment and eased domestic liquidity1 conditions, more urgency may be needed in implementing the reform programme. This column aims to both highlight the broader trends in the economic conditions in India, and infer what policy actions and continued reforms are necessary to put the economy on the right track.

Figure 1. GDP growth rate (%)

Source: CEIC

Source: CEIC

Figure 2. Investment in projects under implementation

Source: Center for Monitoring Indian Economy (CMIE)

Source: Center for Monitoring Indian Economy (CMIE)

Sluggish growth and high inflation

India faces a variety of short-term policy challenges, key among which is sluggish growth and high inflation. GDP growth slowed sharply to 4.5%2 in the last quarter of 2012, from 5.3% in Q3. Inflationary pressures remain persistent, despite headline inflation3 easing to 7.3% in the last quarter of 2012 from the highs of 9-10% over the last two years. The moderation was mainly on account of the recent cooling in (volatile) food and fuel prices. Inflation is still significantly above the Reserve Bank of India (RBI)’s comfort zone of 5-6% with underlying inflationary pressures being further supported by the pass-through effects of higher regulatory prices remaining incomplete4. Going forward, inflation expectations and core inflation5 are likely to remain elevated, limiting the scope for easing by the RBI to support GDP growth.

Rising deficits

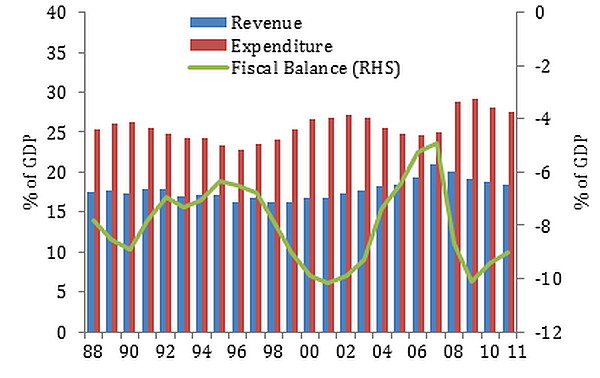

India’s twin fiscal and current account deficits have worsened in recent years. First, the twin deficits create a level of vulnerability for India that is a cause for concern. India’s expansionary fiscal policy (increase in government spending) to fight the 2008 global financial crisis has led to a dramatic deterioration in the country’s fiscal situation. Government spending in the form of several social programmes (particularly the Mahatma Gandhi National Rural Employment Guarantee Program (MNREGA)) has strained the government’s budget position, causing the overall fiscal deficit to widen from 4% in FY62007-2008 to 7% in FY2011-2012 (Figure 3). In the current financial year (2013-14), a fiscal deficit of 5.3% of GDP (an improvement over last year’s 5.8% of GDP) is targeted but the risks of slippage are high, given weaker tax revenue, disappointing proceeds from divestments and 2G auctions, as well as the larger-than-budgeted subsidy bill. This is despite recent reform efforts by the government to increase regulated diesel prices and reduce plan7 and non-plan expenditure. The elections scheduled for 2014 pose the risk of further increasing the fiscal deficit, should political pressures stall these reforms and result in increased spending on social programmes and domestic subsidies.

Figure 3. Fiscal Revenue, Expenditure and Deficit

Source: Ministry of Finance, CEIC

Source: Ministry of Finance, CEIC

The government has announced a fiscal consolidation8 path to reduce the fiscal deficit to 3% of GDP by FY 2016-2017 but the details of how it will achieve this are unclear. India’s fiscal deficit remains one of the highest in the region and this limits its ability to use counter-cyclical policy9 to attenuate the growth slowdown. Although India’s high fiscal deficit constitutes a key vulnerability, there is no immediate financing problem since it is funded primarily by domestic banks and other non-financial institutions like pension/ insurance funds. However, the high deficit does dampen investment activity as it reduces the availability of credit for private firms. Fiscal consolidation is therefore a pre-requisite for an upturn in the credit cycle.

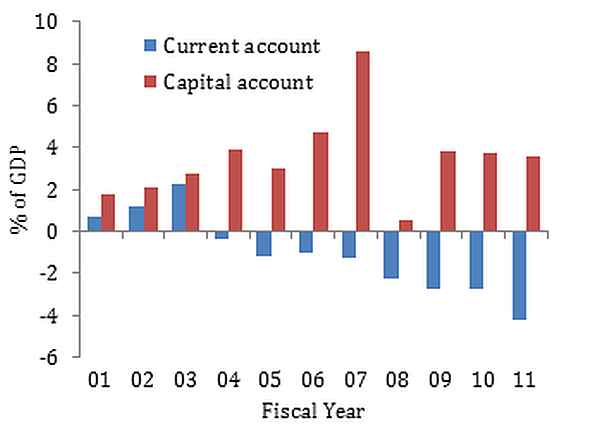

The widening current account deficit (CAD) also remains a major source of concern. While the approach of stimulating domestic demand via fiscal expansion in 2008 put India’s economy back on track after the global financial crisis, the inertia in withdrawing stimulus had subsequently led to a spike in inflation that prompted monetary policy tightening10, and dampened aggregate demand. Gross investment (especially private) and savings slowed as a result. Total savings declined from the peak of 36.8% in FY2007-2008 to 32.3% in FY2010-2011. This decline of 4.5% of GDP exceeded the fall in gross investment of 3% of GDP during the same period. Reflecting the widening gap between savings and investment, India’s CAD increased in the post-credit crisis period (Figure 4). The decline in total savings, a large part of which stemmed mainly from the erosion in public savings due to falling government revenues, has pushed the CAD to the highest level since the 1991 balance of payments (BOP) crisis. During the 12 months ending March 2012, India had a CAD of $78.2 billion or 4.2% of GDP, which widened to 5.4% in the third quarter of 2012. This diverged from the -0.5 to -2% of GDP during 1990-2000, which policy makers have been conservatively maintaining since the 1991 BOP crisis. Historically, India has run a CAD primarily due to the policymakers pushing investments and growth higher than that supported by the domestic saving rate. After FY2008-2009, however, savings have been declining at a much faster rate than investment.

Figure 4. Current and capital account

Source: CEIC

Source: CEIC

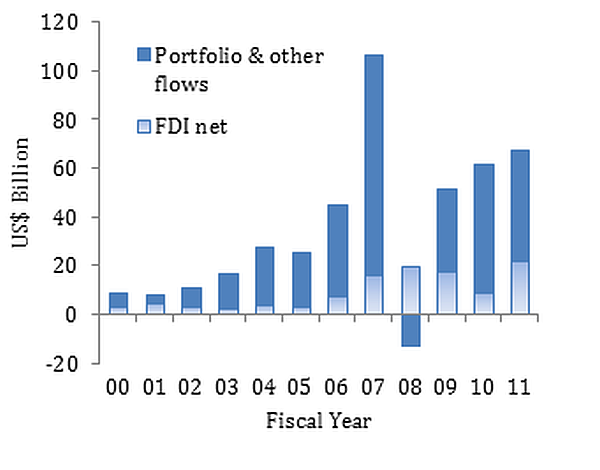

A widening CAD could potentially lead to pressures on the country’s BOP and the currency. Although India’s CAD has been offset by capital account surpluses, nearly three-quarters of the deficit for the past four years was estimated to be funded by more volatile sources of capital, including commercial loans, trade credit and portfolio equity and debt inflows (Figure 5). Considering India’s high CAD, the risk of slowdown in capital inflows will exacerbate the funding risks and currency depreciation pressures. India’s rising CAD raises serious questions about its sustainability, particularly against the backdrop of volatile global conditions and volatile capital flows. The RBI had carried out an analysis showing that with GDP growth of 7%, a CAD-GDP ratio of around 2.5% is sustainable. With India’s CAD already exceeding this threshold level, its external vulnerability is expected to rise further.

Figure 5. Net capital inflows

Source: CEIC

Source: CEIC

Need for concerted policy action

India will need better macroeconomic performance and concerted policy action to fundamentally tackle the twin deficits as well as elevated inflation. To continue to improve the economic environment, a number of reforms in infrastructure, fiscal and financial areas are crucial. The reforms thus far have focused on increasing FDI, raising administered prices to reduce the fiscal deficit, restructuring the power sector etc. While the significant structural reforms require Parliamentary approval, the ones more likely to go through are those that require executive decisions11. For instance, key bills that could be introduced include the Land Bill, the Pension and Insurance Reform Bills and the new Companies Act (Table 1). If these are implemented, they would provide some impetus to an economy that needs more than just a good start to the reform process.

Table 1. Structural reforms reliant on Parliamentary approval

|

Sector |

Reform |

Objective |

Parliament approval |

Likelihood |

|

Fiscal |

Medium-term fiscal consolidation

Disinvestment

Subsidy transfer

Goods & Services Tax (GST)

Direct Tax Code (DTC) |

Long term deficit of 3% by FY2016-2017. Across the board cuts in plan and non-plan expenditure

8 companies notified. FY 2012-2013 target may be raised from Rs. 300 bn ($5.5 bn approx.)

Direct cash transfer, based on Unique Identification Number system

National value-added tax on goods, services to replace multiple layers of taxation

To rationalise direct taxes |

X

X

X

√

√ |

Less likely

Ongoing

Ongoing

Less likely

Less likely |

|

Infrastructure |

Fast-track Infra Projects

Railways

National Manufacturing Policy

Road projects

Coal availability

Land Acquisition Bill |

Establish National Investment Board to fast-track infrastructure projects over Rs. 10 bn ($18.5 million approx.)

Hike in tax fares

To increase manufacturing growth to 12-14% per year

Target of awarding 8800 km road projects in FY2012-2013

To pool imported coal price with that of domestic coal to meet domestic demand

To ease the process of acquiring land for investment projects at fair prices |

X

X

X

X

X

√ |

Likely

Likely

Likely

Ongoing

Ongoing

Less likely |

|

FDI |

Insurance, Pension

Banking licenses

Abolition of short-term capital gains tax

Insurance

|

To increase FDI into insurance to 49% from the existing limit of 26%, and in pensions

To allow entry of new private banks and make sector more competitive

Abolition of short-term capital gains tax which is currently at 15%

To allow reinsurance business, lowering capital requirement for health insurance firms and allowing insurance companies to invest in non-AAA rated bonds12 |

√

√

√

√ |

Less likely

Less likely

Less likely

Less likely

|

|

Others |

Boost public investment through cash-rich state companies

Companies Bill

Mines and Minerals Bill |

To ensure cash-rich state companies to stick to investment targets

To improve transparency and regulation of business houses

Ease supply bottlenecks in the sector and profit sharing of coal companies with local population |

X

√

√ |

Likely

Likely

Less Likely |

Source: Media reports, GS Global ECS Research

Concluding thoughts

The government’s recent moves to improve the deteriorating growth-inflation trade-off is a good start and step in the right direction, but it will be some time before investment fully recovers to lift growth. India’s economy still faces significant challenges in the form of elevated inflation and the ugly twin deficits. Despite the weakening of growth momentum, inflationary pressures have persisted, driven by high commodity prices as well as structural demand and supply imbalances13. Inflation expectations14 are also expected to remain sticky15, creating not merely a risk of further increase in inflation in the near future but also likely to lead to a surge in gold imports (which was a key factor worsening the CAD over the last two years) to protect from inflationary pressures. The persistent fiscal deficit and the declining rupee pose potential threats for further inflationary pressures.

Clearly, ongoing structural reforms are important to rectify the macroeconomic imbalances and to stimulate investment. High inflation has complicated the RBI’s management of the rupee, while the twin deficits significantly limit the monetary space for more aggressive countercyclical policy measures. Infrastructural investments need to increase in order to alleviate supply bottlenecks and bring about non-inflationary growth. Thus far, it is a good sign that the government is finally biting the bullet and embarking on reforms to restore confidence. However, much more still needs to be done and reforms should be sustained in order to lead to a more meaningful improvement in India’s macroeconomic environment.

Notes:

- Liquidity basically refers to the cash or money available in the economy. The Reserve Bank of India (RBI) is the sole supplier of liquidity in the economy. The supply of liquidity by the RBI depends on the public’s demand for currency, and the banking system’s need for reserves to settle or discharge payment obligations.

- On an year-on-year basis.

- Headline inflation is a measure of the total inflation within an economy and is affected by areas of the market which may experience sudden inflationary spikes such as food or energy.

- The RBI warned in its latest monetary policy report that the the indirect impact of the diesel price hike in September 2012 remained contained, indicating that firms did not pass on rising input costs to output prices on account of weak demand conditions. In mid-September 2012, diesel prices were raised by 12% while minimum support prices for food have been raised between 15-40% last year. Further, 18 states have increased electricity tariffs, the latest being Uttar Pradesh, India’s largest state, which has raised prices by about 18%. Reforms in the coal sector will also likely lead to coal price increases in the near future.

- Core inflation represents the long run trend in the price level. It excludes items frequently subject to volatile prices, like food and energy.

- Financial Year.

- The Plan expenditure is the government spending on social sector schemes. It also includes the Centre’s assistance to states and Union Territories.

- Fiscal consolidation refers to a conscious policy effort is by the government to live within its means and thereby bring down the fiscal deficit and public debt. It includes, among other things, efforts to raise revenues and bring down wasteful expenditure.

- Counter-cyclical policy is defined as a measure or tool implemented by the government to combat economic episodes like recessions that are caused by cyclical factors, for instance, a downswing in business cycles that adversely affect domestic investment and consumption etc. Examples of such counter-cyclical policies could be a rise in government expenditure on infrastructure in order to generate jobs and stimulate consumption, lowering of corporate taxes for businesses etc.

- Monetary policy tightening aims to reduce the supply of money in the economy.

- Goldman Sachs, “India’s reforms: Well begun, but not half done”, Asia Economics Analyst, Issue No: 12/19. 1 Nov 2012.

- The credit rating of a bond assesses the credit worthiness or the ability to meet financial obligations/ commitments of the entity issuing the bond. AAA signifies the highest degree of credit worthiness.

- Higher demand due to shifting dietary patterns and rising household incomes have led to higher food prices, which are further exacerbated by low agriculture production growth that has averaged less than 2% per annum in the past decade.

- Inflationary expectation is the rate of inflation that workers, businesses and investors think will prevail in the future, and that they will therefore factor into their decision making. For instance, if a worker expects inflation to be high, he/ she may demand higher wages to keep up with the rising prices. Hence, inflation leads to inflationary expectations that lead to further inflation.

- Slow to change.

Further Reading

- IMF (2011) ‘India Sustainability Report’, G20

- IMF Staff Report for the 2010 Article IV Consultation. Report can be accessed at http://www.imf.org/external/pubs/ft/scr/2011/cr1150.pdf.

- Reserve Bank of India, Macroeconomic and Monetary Developments, Third Quarter Review, 2012-13.

Comments will be held for moderation. Your contact information will not be made public.