13 May, 2013

13 May, 2013

In the world’s second-most populous country, it is unsurprising that the topic of energy supply should be a key issue – and, in particular, its sustainability. This column completes a series on India’s energy challenges. It argues that sustainable energy supply and continued rapid economic growth of India can be compatible.

The scope for improvement in India’s energy system is vast. Renewable energy currently makes up a negligible share (0.36%) of total primary commercial energy supply while 96.9% of such supplies come from fossil fuels and 2.76% from hydro and nuclear resources. The non-commercial combustible biomass and wastes which contributes to the extent of 24.5% of the total energy supplies are excluded in this balance. This column outlines the state of renewable energy in India and what can be done about it.

The state of renewables

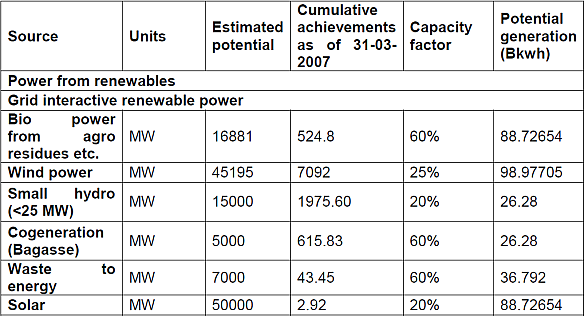

The most important application for new alternative energy resources, such as wind, solar, micro-hydel, biomass and waste, is in the area of electric power generation. Wind energy, solar thermal as well as solar photovoltaic electric energy (that which comes from solar radiation)have substantial potential in India as shown in Table 1. Wind power can be generated from the energy potential of on-shore wind flow on a cost-competitive basis, but only at a low-load factor of about 20%. Solar thermal energy, on the other hand, is an economically feasible option mainly for water heating. The solar photovoltaic power is still a high-cost option, with cost per unit being in the range of Rs. 15 to 20/kwh. However, the development of solar thermal power involving the use of high temperature collectors with mirrors and lenses, and steam turbine is underway and could add substantial potential power generation in the future. Table 1 shows the estimated potential of power capacity and the cumulative achievement of installation as of 31 March 2007 as per India’s ‘Eleventh Five Year Plan’ document along with alternate assessments obtained from other sources, which can be used for realistic energy planning in the medium to long run.

Development in the use of these renewable energy sources has, until now at least, been poor. The lack of entrepreneurship in the deployment of such capital and technology, lack of institutional support at the grass-root level, poor focus on training and management for using and maintaining such new technologies and the lack of awareness of the rural community – on top of the high cost – have been key barriers.

Table 1. Estimated medium-term (2023) potential and cumulative achievement

Source: Eleventh Plan Document (Planning Commission), Expert Group on Low Carbon Strategies for Inclusive Growth of the Planning Commission (2011) and interview with World Institute of Sustainable Energy (WISE) in 2012.

Source: Eleventh Plan Document (Planning Commission), Expert Group on Low Carbon Strategies for Inclusive Growth of the Planning Commission (2011) and interview with World Institute of Sustainable Energy (WISE) in 2012. Primary commercial energy requirement and CO2 emissions in the long run

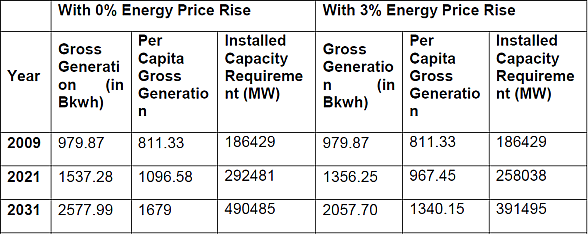

If it were possible to remove the above barriers to the deployment of such technologies, how much could we expect the future scenario of primary energy projections for India to show a lowering of dependence on fossil fuel, particularly coal? And how far could primary commercial energy intensity of GDP and CO2 intensity of GDP be reduced over a long-run planning horizon like 2031-2032? Keeping in view of the potentials of new renewables, I submit below possible (though not optimum) scenarios of energy and CO2 emission projections based on my recent research (Sengupta 2012). The study assumes alternative combinations of annual GDP growth rates of 8% and 6% per year combined with two scenarios of real energy price rise (through taxation) – 0% rise and 3% rise per year over the base year of 2009-2010 for the entire time horizon. The assumptions about the fuel composition of final energy demand in the different non-energy sectors showing increasing penetration of electricity would yield the projection of total final demand for electricity at the consumer end over time. The aggregate gross generation requirements of electrical energy are derived for such final demand estimates by adjusting these for the factors of auxiliary loss, and transmission and distribution losses. The projections for such future gross generation requirements are given for 8% growth rate in Table 2.

Table 2. Gross generation of electricity (in Bkwh) for 8% GDP growth

Source: Author’s own calculations

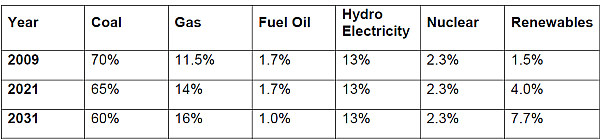

Source: Author’s own calculations In order to estimate the total future requirements of individual fuels of the different sectors directly and indirectly through power, the study considers two fuel mix scenarios for the gross generation of electricity. The base line one assumes the business-as-usual growth of share of new renewables in the total gross generation of electricity with some moderate challenges so as to reduce the share of coal in thermal generation from 70% in 2009-2010 to 60% in 2031-2032. The second scenario, on the other hand, where development of new renewables is accelerated, assumes a much higher rise in the share of renewables in power generation such that the share of coal can be brought down to 50% by 2031-2032. In both the scenarios we have tried to keep within the realms of realism by setting the shares of new renewables as substantially lower than what the National Action Plan of Climate Change has targeted due to the slow pace of their adoption in the Indian energy industry. Table 3 shows the fuel composition of electricity generation as per the base line scenario, while the shares of coal and renewables in the scenario of accelerated introduction of new renewables are 60% and 9.4% respectively in 2021-2022 and 50% and 17.7% in 2031-2032 and those of all other fuels remains the same as in the base line fuel composition scenario.

Table 3. Share of fuels in electricity generation – baseline growth in electricity from renewables

Source: Author’s own calculations

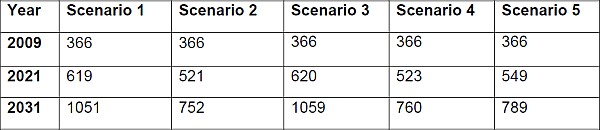

Source: Author’s own calculations We then look at the growth in the total requirement of primary commercial energy supply and total CO2 emissions of India and their respective intensities with respect to GDP over the time horizon up to 2031-32 for the following five scenarios (see Tables 4 to 7):

- Scenario 1 (baseline): 8% GDP growth rate, 0% annual rise in real energy price, baseline use of new renewables

- Scenario 2: 8% GDP growth rate, 3% rise in real energy price per year, baseline use of new renewables

- Scenario 3: 8% GDP growth rate, 0% rise in real energy price per year, accelerated use of new renewables

- Scenario 4: 8% GDP growth rate, 3% rise in real energy price per year, accelerated use of new renewables

- Scenario 5: 6% GDP growth rate, 0% rise in real energy price per year, baseline use of new renewables

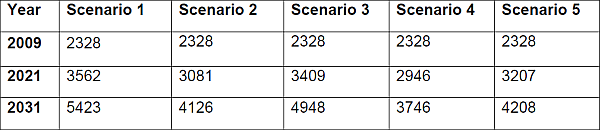

Table 4. Total primary commercial energy requirement (MTOE)

Source: Author’s own calculations

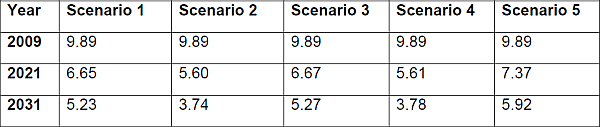

Source: Author’s own calculations Table 5. Primary commercial energy intensity of GDP (goe/ rupee)

Source: Author’s own calculations

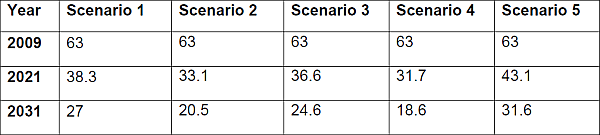

Source: Author’s own calculations Table 6. Total CO2 emission (Mill.Tonne)

Source: Author’s own calculations

Source: Author’s own calculations Table 7. CO2 emission intensity of GDP (gm/rupee)

Source: Author’s own calculations

Source: Author’s own calculations

It may be further noted that the individual fuel requirements of scenario 2 (with energy price rise through taxation) and scenario 4 (with both energy price rise and accelerated use of new renewables) in the projections though not presented here would show reduction in the pressure on fossil fuel demand and abatement of CO2 emission substantively vis-à-vis the baseline scenario. These would contribute to reduce the pressure on coal and oil energy import substantively for any terminal year. The requirement of coal will in fact go down from the baseline figure of around 1,100 million tonnes in 2031-2032 to 790 million tonnes in 2031-2032 and that of oil similarly from around 1,000 million tonnes to 615 million tonnes by 2031-2032 as per scenario 4.

Regarding the adequacy of supply electricity from new renewables to meet the requirements of the projections, there should not arise any serious problem as the least estimate of such requirements from new renewables has been 433 billion units in 2031-2032 for the various 8% GDP growth scenarios, which exceeds the generation potential estimate of 366 billion units by the grid connected interactive supply from such sources. The shortfall should be met from off-grid units of the power supply without difficulty as the latter is supposed to have a huge potential in India.

Concluding remarks

My normative projections suggest that the total CO2 emission, which is supposed to be responsible for the carbon footprint, will rise from 2.3 billion tonnes in 2009 to somewhere in the range of 3.7 billion to 5.4 billion tonnes in 2031-2032 if there is 8% GDP growth depending on the assumptions of the other policy variables of real energy pricing, penetration of electricity and the share of new renewables in the fuel mix of power generation. It may be noted that the Integrated Energy Policy Committee Report of the Planning Commission projected a total primary commercial energy requirement and the supporting supply to meet this, for an 8% growth rate under alternative assumptions that had implied the total CO2 emission to vary in the range of 3.9 billion tonnes to 5.5 billion tonnes in 2031-2032. As the results of these two studies are not much different, it suggests a robust conclusion that India would be able to substantively weaken its CO2 emission-growth linkage by reducing the CO2 intensity of GDP in the coming decades. However, among the policies, 8% growth along with real energy price rise through fiscal taxation at the rate of 3% per year gives us the least estimate of primary energy intensity of GDP (that is of 3.74 gm/ rupee) while the low growth (6% per year) strategy with no price rise will give us the highest primary energy intensity of GDP (that is 5.92 gm/ rupee) by 2031-2032. The comparative projections further show that decelerating the growth rate of an economy is an inefficient strategy for conserving the bio-capacity or reducing the carbon footprint as compared with price (tax) induced energy conservation or to the enforcement of power generation by new renewables.

Further reading

- Sengupta, R (2012), ‘Green Economic Development and India’s Energy Policy Questions’, Report of a Study for the Climate Finance Unit of the Department of Economic Affairs, Ministry of Finance, Government of India, December.

Comments will be held for moderation. Your contact information will not be made public.