25 June, 2021

25 June, 2021

The government and the Central Bank have undertaken various measures to protect the banking and finance sector from the adverse impact of the Covid-19 crisis. However, despite historically low interest rates, credit growth has been rather low in recent quarters. In this post, Harsh Vardhan discusses the long-term, structural issues with credit in India, and its crucial role in ensuring sustained economic recovery.

The Covid-19 pandemic has put the Indian economy in deep trouble. Estimates of contraction of GDP (gross domestic product) for the 2020-21 Financial Year range between 7.5% and 10%. The much more virulent second wave, which began in April 2021, has dampened the prospect of rapid recovery from the economic slump, and it is still unclear when complete normalcy will return. The banking and finance sector in India always bears the most direct impact of economic fluctuations. It is also the most important driver for economic recovery; nearly 70% of the fiscal stimulus announced by the government last year was to work through the banking system with schemes such as credit guarantees. Good health of the banking system is critical to ensure that the Indian economy exits the pandemic on a strong growth trajectory. The government and the banking regulator have taken several measures to protect banks from the likely impact of the pandemic, including a moratorium1 on loan repayments, credit guarantee schemes, and suspension of the bankruptcy code. The Central Bank has used monetary policy tools – both conventional and unconventional – to maintain high liquidity in the financial system, keep interest rates down, and provide funding to banks through targeted repo2 operations so that they could provide credit to stressed sectors. All these measures have protected the banking system from having to show a sharp increase in bad loans, so far. They have also helped improve credit flow to some hard-hit sectors. However, despite historically low interest rates, credit growth of the banking system has remained anaemic, at around 6% for the last several quarters, which raises some deeper questions about credit in Indian economy. The Covid-19 pandemic has compelled policy and regulatory attention on the more immediate issues and responses to them, in a firefighting mode. As the pandemic recedes, it will be important to focus on the long-term and structural issues with credit in India.

Structural collapse of commercial credit

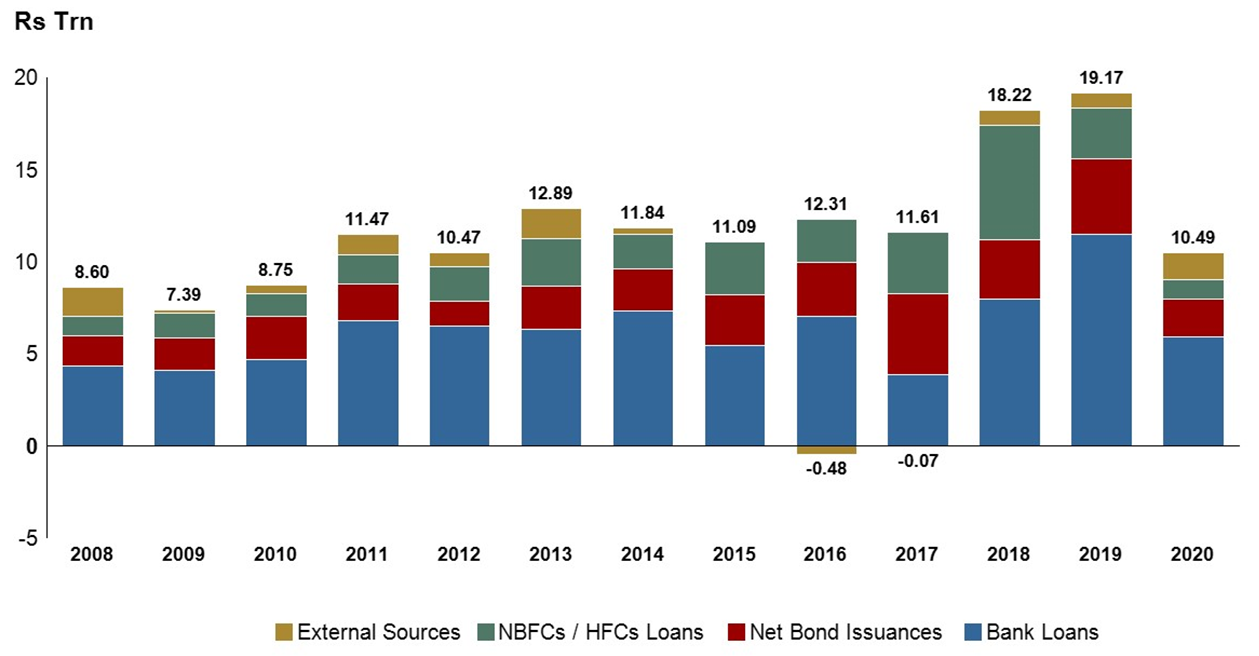

Commercial credit flow, that is, incremental credit to businesses and individuals, has remained essentially stagnant in India for over a decade. Figure 1 below shows the commercial credit flow in India from financial years 2008 to 2020. It breaks down the flow of credit across its four main sources: banks, non-banking finance companies (NBFCs, including Housing Finance Companies (HFCs)), issuance of bonds, and external sources mainly including external commercial borrowings by companies.

Figure 1. Flow of commercial credit in India

Source: Reserve Bank of India (RBI).

Note: NBFC/HFC credit to business is net of bank credit to them.

Figure 1 above shows that the annual flow of such credit has remained around or below Rs. 12 trillion for all the years in the decade 2011-2020 excluding 2018 and 2019. Compounded annual growth rates (CAGR) of credit flow from banks and NBFCs over this period are -1.8% and -4.5%, respectively, while CAGR of net bond issuances is 0.8%, and for external sources of credit is 3.4%. The shares of the various sources in the flow of credit have also fluctuated. Banks, which have historically been the largest providers of credit in India, saw their share peak at about 62% in 2014, and declined to below 35% by 2017 largely due to bad loan cycles, and regulatory actions such as the asset quality review (AQR) by the RBI in 2016. Bond issuances and NBFCs’ credit filled the gap left by banks and their share in the same period rose from 20% to 37%, and from 20% to 30%, respectively. The IL&FS (Infrastructure Leasing and Financial Services) episode in September 2018 led to a sharp decline in the share of bonds and NBFCs, which fell to 20% and 10%, respectively, by the Financial Year (FY) 2019- 20. Banks’ share went back up to about 56%.

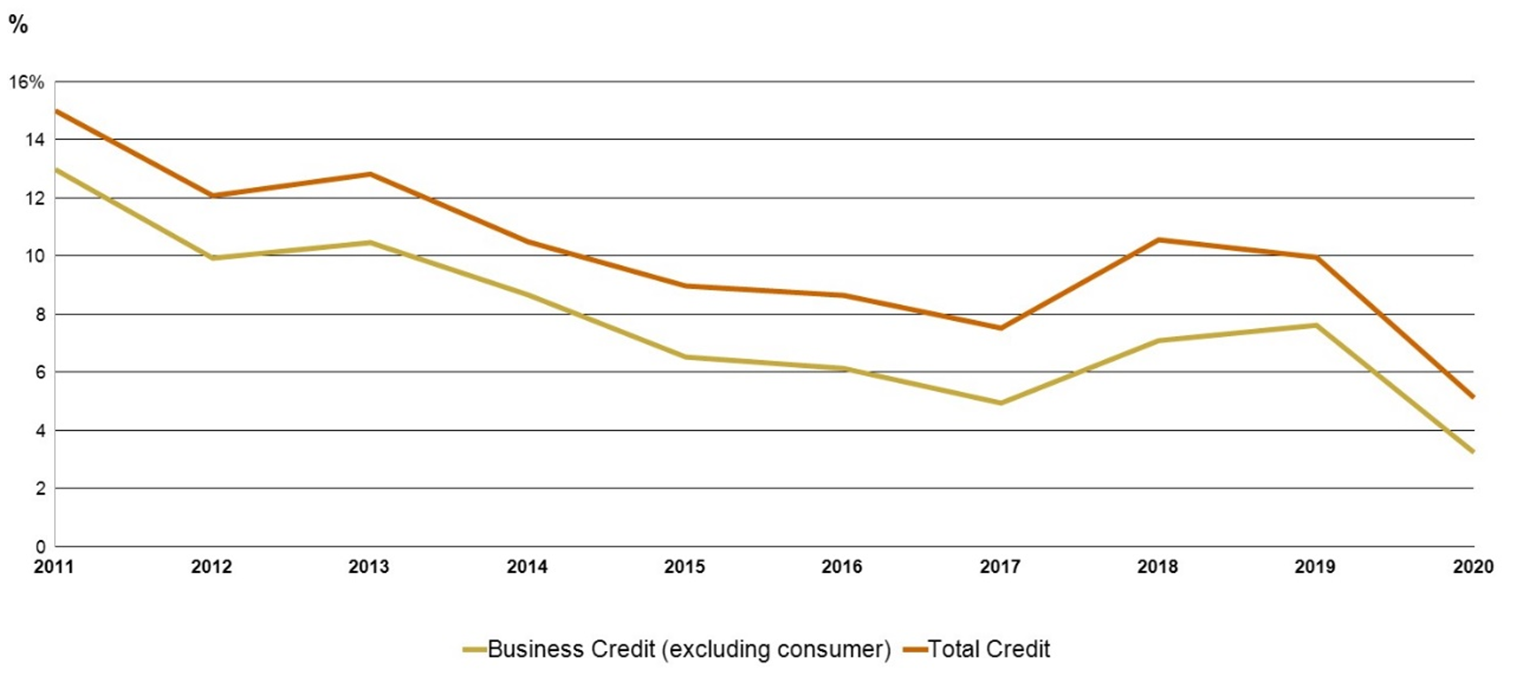

While in absolute terms, the flow of credit appears almost stagnant over the past decade, as a percentage of nominal GDP it shows a real worrisome picture. Figure 2 presents the ratio of flow of credit as a percentage of nominal GDP. The ratio is mapped for total credit and for business credit, that is, subtracting consumer credit from total credit.

Figure 2. Commercial credit flow as a percentage of nominal GDP

Source: RBI.

Note: Exact data for consumer credit are available in the public domain for banks but not for NBFCs; for NBFCs, 25% of the credit flow is assumed to be to consumers.

It is customary to look at the ratio of total credit to GDP, which is essentially ratio of a stock measure (total credit) with a flow measure (GDP). Here, we look at ratio of incremental credit to GDP which is ratio of two flow measures.

Figure 2 shows that as a percentage of nominal GDP, total flow of credit has fallen from a level of 15% in 2011 to about 5% in 2020. The ratio for business credit has fallen from about 13% to 3% over the same period. Data on this ratio are not available for a longer time-series but it is reasonable to conclude that this is the lowest level of the credit flow to GDP ratio since economic liberalisation in 1991. Compounded annual banking credit growth has been 10.6% for this decade. For the 2020-21 Financial Year, banking credit growth was approximately 5.5%, which was close to a seven-decade low.

What has caused this slump in credit?

There are several factors affecting the demand and supply of credit that would drive the slump.

Demand factors: Two sources drive demand for credit from the private sector – growth in investments in new production capacity, and growth in working capital as businesses grow. Demand from both these sources fell in the last decade. In the earlier decade (2001-2010) there was an investment boom which included, chiefly, investments in infrastructure. Some of these infrastructure investments suffered a host of problems and credit given for them turned bad, causing an overall souring of sentiments. There was also a demand slowdown that started at the beginning of the last decade. Data from CRISIL (Credit Rating Information Services of India Limited) show that average capacity utilisation from 2011 to 2020 for manufacturing companies remained between 65% and 75%. At this level of capital utilisation, no fresh capacity addition makes sense.

In addition to a slow-down in credit demand for investments involving capacity addition, credit demand for working capital also tapered. This was mainly due to two factors – improving efficiency of supply chains and low wholesale price index (WPI) inflation. Over the last decade, investment in information technology and infrastructure (highways, communications, etc.) have resulted in significant efficiency gains in the supply chains of the private sector resulting in lower inventory levels and receivables, and reduced cash holdings. For the whole decade, WPI inflation averaged at below 2% suggesting very low pricing power with businesses. The combined effect of supply chain efficiency and low pricing power meant that the working capital needs of companies grew much more slowly than business volumes.

The Insolvency and Bankruptcy Code (IBC), which was passed in 2016, brought in sweeping changes to how corporate bankruptcy was dealt with in India. It strongly established creditors’ rights, and for owners of firms, created a very real possibility of losing control of their firm due to bankruptcy. In the earlier regime, owners could dodge loan defaults as the rights of creditors were limited. As a result of this new law, firms became much more cautious about borrowing and overleveraging.

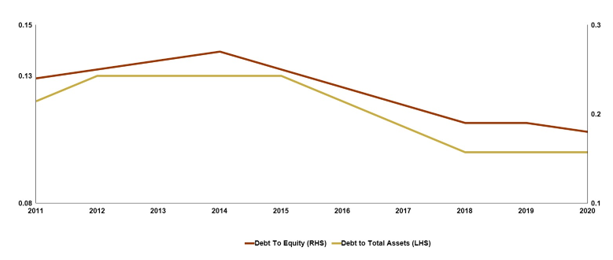

The combined effect of these factors was a wave of deleveraging for Indian firms. Large companies systematically reduced their leverage. Figure 3 below presents key leverage ratios for the top 200 non-financial firms by market capitalisation for the period of 2011 to 2020. It shows that leverage measured as ratio of debt to equity and debt to total assets declined in this period. The decline is especially sharp after the 2015 Financial Year.

Figure 3. De-leveraging of large corporations

Source: Prowess.

Buoyant public equity markets and strong investments by private equity firms aided this process, as companies could easily raise equity capital to reduce debt levels.

Supply factors: The most important contributing factor on the supply side for the collapse of credit was the widespread risk aversion among banks. By 2012 or so, bankers began to sense the growing non-performing loans (NPLs) on their books and became much more conservative in lending. The average annual growth of banking credit for 2001-2010 was 23.6%. It dropped to below 10% by the 2014-15 Financial Year, and while 2018 and 2019 saw some uptick in credit growth, it fell back in 2020. For 2011-2020, the average annual growth in banking credit was 11.7%, half of what it was in the previous decade.

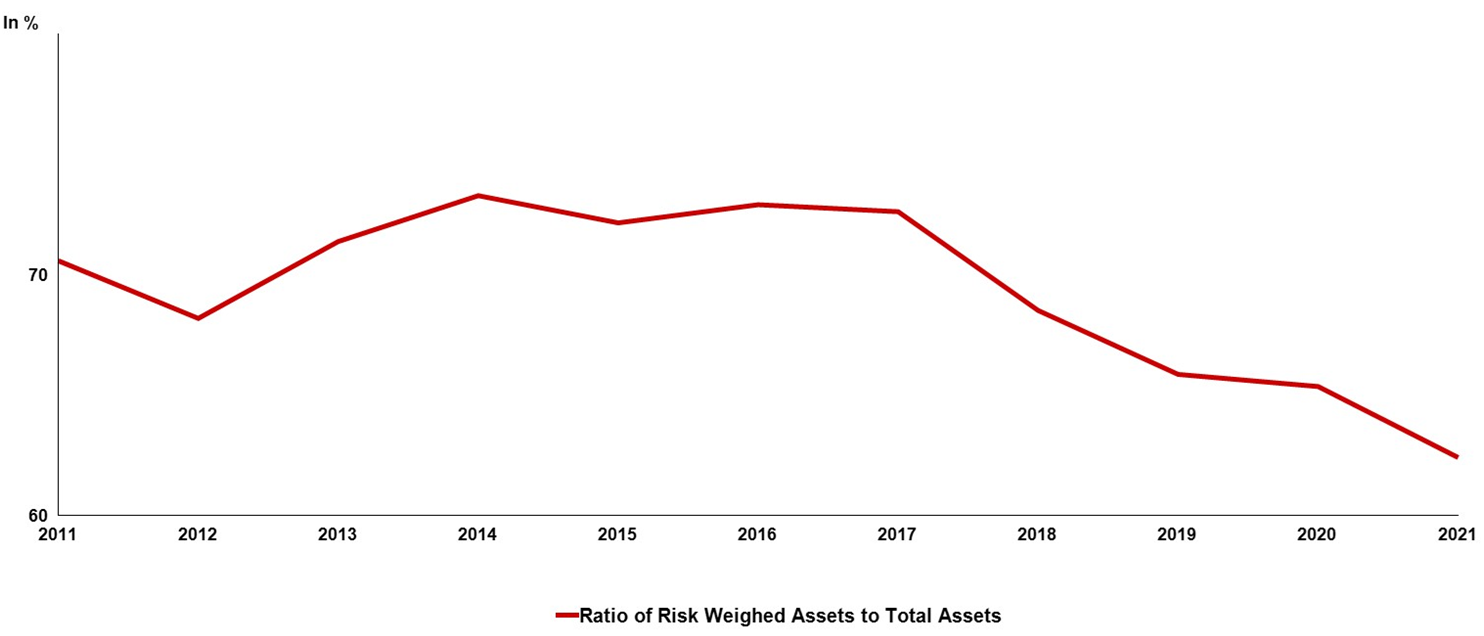

A simple indicator of the risk aversion in Indian banking is the risk weighted assets3 (RWA) density of the banking system. Figure 4 shows the RWA density for 12 Indian banks, accounting for over 80% of total banking assets.

Figure 4. Risk aversion in Indian banking

Source: Bank disclosures.

Figure 4 shows that Indian banks lowered the riskiness of their loan portfolio after 2014, and very sharply post 2017. This was achieved mostly by moving lending from industrial customers to much lower risk-weight carrying consumer loans such as mortgages, and also by higher investment in government bonds.

As banks experienced rising NPLs on their corporate lending, they responded by redirecting their incremental lending to consumers and indirectly lending through NBFCs. While the CAGR for banking credit as a whole was 10.7%, it was 15.5% for consumer loans, and 19.3% for loans to NBFCs. The share of industry in banking credit went down from 43% in 2011 to 31.4% in 2020, while that for consumer loans went up from 18.7% to 27.6% during the same period. The share of NBFCs in banking credit doubled from 4.9% in 2011 to 9.8% in 2020.

Fall in banking credit to businesses was made up, to some extent, by bond issuances and credit from NBFCs. From 2014 until 2018, both bond markets and NBFCs contributed significantly to credit flows. Interest rates in India secularly declined from July 2013, and ample liquidity in the system helped bond-issuers and NBFCs. However, the default on bonds by IL&FS – among India’s largest NBFCs – in September 2018, brought this to an abrupt stop. Default from such a well-established and highly rated (AAA) NBFC created panic in the bond markets and raised questions about the NBFC business model.

The bond market has recovered from the IL&FS episode, but is extremely skewed. There is no investor appetite for bonds rated A and below. Even among the top-rated (AAA) bonds, a large share of issuances is by government-owned entities. Insurance and pension funds are the largest pools of capital that invest in bonds and while they have been permitted to invest in bonds rated A, they have not invested meaningfully in bonds below AA+ rating. Hence, while the overall bond issuances have increased in value, issuing bonds as a funding option is currently open to only a handful of highly rated companies. NBFCs were a source of credit to many businesses, especially micro, small and medium enterprises (MSMEs) that were shunned by banks. Banks were happy to lend to NBFCs, who in turn would lend to these businesses; capital in the NBFCs provided a sort of first-loss default guarantee4 to banks. Post the IL&FS episode, most NBFCs, excluding a few highly rated ones, suffered from lack of liquidity from both the banking system and the bond market, and hence, reduced their lending.

Re-energising credit for sustained economic recovery

India is often described as an ‘investment-led’ economy. Given its stage of development, sustained investment is needed for sustained economic growth. Availability of credit is a prerequisite for investments. Various measures announced by the government and the RBI to deal with the impact of the pandemic, are necessary and useful. They would help banks remain on an even keel as the economy recovers. However, to ensure sustained growth, that is, real GDP of over 7%, which is widely accepted as the aspiration for India, the structural collapse of credit over the last decade will have to be addressed. The FY 2020-21 will show an increase in the credit flow to nominal GDP ratio because of the denominator effect, that is, a contraction in the nominal GDP. In order to get back on to a robust growth strategy, credit flow will have to increase significantly. Both the demand- and supply-side issues highlighted in this post will have to be addressed in order to achieve a sustained improvement in credit flow.

On the demand side, the pent-up demand from the lockdown could increase capacity utilisation, and trigger new investments. Hence, a revival of the investment cycle is critical. Businesses will have to start investing in new capacities. Globally, there has been a revival of capital expenditure as economies are emerging out of the pandemic and we can expect a similar revival in India as well. The biggest boost to investment, however, would come from fiscal stimulus. A key component of credit growth over the last few quarters – albeit languid – has been assumed to have come on the back of spending by government agencies such as the National Highways Authority of India (NHAI). Continued spending by the government directly and through its agencies, could result in a trickle-down effect on downstream industries and push investments. Furthermore, the government must take steps to encourage private sector investments by ensuring that the factors that adversely impacted the investments in the earlier decade are addressed. The current uptick in WPI inflation, could restore pricing power to businesses and make them more confident of investing.

Addressing the supply side will also be challenging. Primarily, it will require a restoration of risk appetite among bank managements, especially of the government-owned (public sector) banks. Over 60% of share of banking credit is with the PSU banks. The Covid-19 pandemic hit just as these banks were emerging out of the devastating NPL cycle they had been through in the past few years. The government had invested over Rs. 3 trillion to recapitalise these banks. The impact of the pandemic and the lockdowns on these banks is unclear as India is still facing the second wave of Covid-19. It is reasonable to assume that the pandemic and its expected impact will increase risk aversion in banks. Unless these banks start lending again, it will be difficult to improve overall credit flow. Improving governance in these banks and encouraging the strengthening of risk management systems will be critical to get these banks to start lending again.

Several committees in the past have made recommendations on the development of the bond market in India. This may be an opportune time to act on those recommendations. While the market has indeed developed quite a bit in the last couple of decades, it has still not emerged as a substitute to institutional credit. It is accessible only to companies with very high credit ratings. Over 85% bonds issued (by value), are rated AA and above. On the other hand, the median rating of a commercial bank borrower is BBB. Cleary, an important challenge is to make the bond market accessible to lower rated companies. A well-capitalised and well-managed credit enhancement institution could play a crucial role here. The government can consider seed-funding such an institution.

The Covid-19 pandemic has posed immense economic challenges and has elicited a strong and comprehensive response from the government and the RBI. While close attention needs to be given to the recovery from the pandemic, long-term structural issues in credit should not be overlooked. The economy may bounce back from the pandemic, but the resulting growth will not be sustained, unless these structural issues are resolved.

The author would like to thank Josh Felman and Rajeswari Sengupta for helpful comments.

I4I is now on Telegram. Please click here (@Ideas4India) to subscribe to our channel for quick updates on our content.

Notes:

- A moratorium on loan payments refers to a period during the loan term when loan payments are not required to be made. On account of Covid-19, the Reserve Bank of India (RBI) permitted lending institutions to bring into effect a term-loan moratorium until 1 June 2020, which was extended to 31 August 2020. The asset classification standstill clause changed the bad loan classification period to 180 days from 90 days for all such accounts.

- The RBI defines repo as “a money market instrument, which enables collateralised short term borrowing and lending through sale/purchase operations in debt instruments. Under a repo transaction, a holder of securities sells them to an investor with an agreement to repurchase at a predetermined date and rate”.

- RWA density is defined as the ratio of RWA to total assets of the bank.

- First-loss default guarantee is the process by which a third party compensates lenders when borrowers default, and as the third party compensates for the default, it makes lenders more confident to give out loans.

By: Ashok Masillamani 13 December, 2021

Excellent presentation with technical analysis, but still lack courage to call the spade a spade. All inclusive structure of Indian economy unlike rest of the world can survive any Pandemic. Political chaos has ruined the unbreakable economy using Pandemic as its cover. This could lead to disintegration of India. I wish that happens sooner.