19 May, 2022

19 May, 2022

The Phillips curve represents an inverse relationship between inflation and unemployment. In this post, Parantap Basu argues that the ‘illusory’ Phillips curve in western industrial nations is driven by a withdrawal from the workforce rather than a demand boom. He contends that now might not be the ideal time for central banks across the world to hike rates, as this has the potential to worsen existing supply-side issues and stagflation.

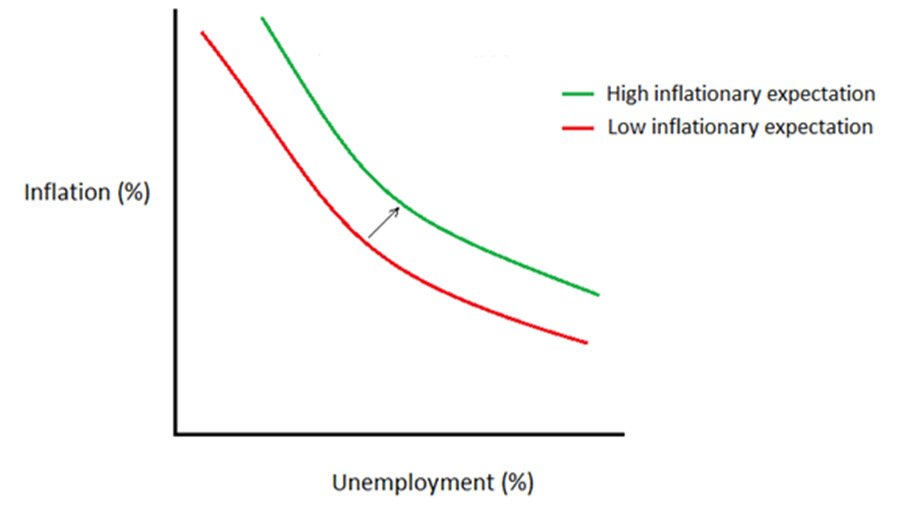

A spectre is haunting the world – the spectre of high inflation. In 1958, a New Zealand-born economist, William Phillips published an article in Economica positing an inverse relationship between wage inflation and unemployment (Phillips 1958). The idea was that when the economy is ‘overheated’ with a high buying spree prompted by general economic prosperity, shops and factories become occupied with catering to this burst of demand. One can see more ‘Help wanted!’ signs in stores, with higher wages being offered, and this also tends to be a period of disappointment for bargain hunters as stores jack up prices. Thus, higher inflation accompanies lower unemployment. This inverse relationship between inflation and unemployment, known as Phillips curve, became the cornerstone of macroeconomics; I would not do justice to teaching my 'Macro 101’ class, without a mention of this curve. However, this curve is not very stable and shifts when people change their expectations of future inflation. For example, when the market expects higher inflation, the curve shifts upward (see Figure 1).

Figure 1. Phillips curve under high and low inflationary expectations

The Phillips curve and central banks

Central banks all over the world take the Phillips curve into account when planning monetary policy. They raise their key interest rates when inflation is high and unemployment is low, as a measure to ‘cool’ the market.1

The US Federal Reserve (Fed) recently raised its benchmark rate by 0.5% – the steepest hike in 22 years. The Bank of England responded to this by increasing its rate from 0.75% to 1% which is the highest level in 13 years since the financial crisis. The European Central Bank has not yet raised the rate from its negative level, but it has confirmed the end of its bond buying programme.

Indian monetary policy and food inflation

The Reserve Bank of India recently raised its repo rate by 0.4%, from its record-low 4% level during the Covid-19 pandemic. This is a surprise move taken ahead of the Fed’s, with an aim to drain liquidity from the banking system. In India, the current Consumer Price Index (CPI) inflation rate is 7.79% (as of May 2022), which is higher than the upper limit of the 2%-6% flexible inflation target range set by the Monetary Policy Committee.

Foodgrains constitute a major fraction of the CPI in India. The Consumer Food Price Index (CFPI) which was 5.85% in February 2022 has increased to 7.68%. Should we worry about this steep rise in food price inflation? Yes, we certainly do. However, there is no need to panic. The mechanics of food price inflation are unique for India and no monetary policy of tinkering with the rate can make a dent on this. It is important to remember that India is a major producer of wheat and rice, and it does not depend on the currently war-stricken Ukraine and Russia for food supply. According to Food Corporation of India data, as of April 2022, the buffer stock of wheat was 1.90 million tonnes, while the strategic requirement of stock is 0.74 million tonnes. For rice, these numbers are 3.23 million tonnes and 1.35 million tonnes, respectively.2 In other words, we have a significant buffer stock of wheat which is still considerably above the minimum stock required. When the market price falls below the minimum support price (MSP) – the minimum price stipulated by the government to support the farmers – the government buys the excess foodgrains from the farmers at this MSP, and builds up the buffer stock.

It is reasonable to expect that the market price of foodgrains will rise due to the Russia-Ukraine War. This may result in middlemen engaging in the speculative hoarding of foodgrains, which could contribute to further rise in food prices. Even so, food price inflation is unlikely to spiral out of control as a social safety net is available under the Pradhanmantri Garib Kalyan Yojana – the government provides five kilograms of foodgrains to each person per month, targetting 80 crore intended beneficiaries – until September 2022. Hence, India has enough food reserves to deal with contingency, Thus shortage of food is not the issue. What we need is an efficient public distribution system.

Is it the right time to raise the rate?

The factors currently driving high inflation differ across countries. In the US, the inflation is primarily due to the tight labour market which is exacerbating supply chain bottlenecks. In the UK, a combination of tight labour market conditions and an energy price shock have contributed to inflation. In EU countries, inflation is primarily driven by a rise in energy prices as 40% of the EU’s gas comes from Russia. According to the Bureau of Labour Statistics, in April 2022, the annual increase in the producer price index (PPI) in the US was 11%. The PPI is a price index based on the prices of producer goods that includes gas and energy, among other goods. A higher PPI thus signals that high inflation in the US is not a demand-driven phenomenon. It is due to supply side factors, which is also exacerbated by people quitting the workforce, leading to tight labour market conditions. The reason for tight labour market conditions in the US is an area of active research. It could possibly be on account of demographic shifts and the Covid-19 pandemic. To fill vacancies, companies are keen to hire workers, and are hence offering potential employees high salary packages. This puts pressure on company costs, giving rise to a wage-price spiral. The situation has become more adverse with Russia-Ukraine oil shock affecting the economy. For India, the food price inflation is mostly driven by the speculative hoarding of foodgrains and an inefficient public distribution system. No tinkering with the policy rate can ameliorate the situation.

Why does the Fed still hike rates when inflation is not being caused by a burst of demand? By raising rates, the Fed signals to the market that it fully intends to control inflation – this is known as ‘forward guidance’.3 In other words, the Fed attempts to lower inflationary expectations so that the Phillips curve shifts downward as seen in Figure 1. However, this effort at forward guidance has not been working as intended. Inflation in the US is still sharply rising despite Fed’s warning that rates will be hiked even further this year. In April 2022, US CPI rose by 8.3%, reaching a four-decade high. A rate hike at this juncture is a bad idea. Borrowing rates will sky-rocket. Loan-hungry enterprises will have a hard time in financing their projects. Investments will drop. Adjustable mortgage rates will rise and so will bankruptcies. It may worsen the supply chain bottlenecks even further. For India, a rate hike will affect small and medium enterprises which are finally recovering from the pandemic.

In western industrial nations like the US and UK, an ‘illusory’ Phillips curve is still present. Inflation in these countries remains high and unemployment remains low, as people are quitting the workforce, on account of the reasons mentioned above. Hence, this inverse relationship between unemployment and inflation is not demand-driven as is generally shown in macroeconomics textbooks.

There is now a credible fear of a global stagflation.4 For India, a stagflation-like scenario is also emerging because growth is decelerating, and unemployment is on the rise. Hence, this would not be the right time to raise rates because it has the potential to worsen the existing supply-related problems and thus deepen stagflation.

The supply chain and oil shock issues are not problems that a central bank can solve. Resolving this requires a careful coordination of fiscal and monetary policy. The fiscal authority can subsidise ailing industries and the resulting deficit needs to be financed by a combination of bond financing and monetisation. The Fed and the RBI should remain open to such possibilities and play down its hawkish stand.

The author would like to thank Ritwik Mazumder for providing valuable insights.

I4I is now on Telegram. Please click here (@Ideas4India) to subscribe to our channel for quick updates on our content

Notes:

- This policy response was popularised by the work of John B. Taylor, a Stanford economist and an economic advisor to Gerald Ford and George W. Bush.

- Data on the strategic requirement of food are compiled by ThePrint based on FCI data.

- For a good description of forward guidance as a monetary policy tool, see Nelson (2021).

- Stagflation indicates that inflation is accompanied by decelerating growth. This scenario was also recorded in the 1970s following the OPEC (Organization of the Petroleum Exporting Countries) oil price increase. This maybe emerging again as growth forecasts are ominously low (Romei and Smith 2022).

Further Reading

- Nelson, E (2021), ‘The Emergence of Forward Guidance As a Monetary Policy Tool’, Finance and Economics Discussion Series 2021-033, Board of Governors of the Federal Reserve System, Washington.

- Phillips, AW (1958), “The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom 1861–1957”, Economica, 25(100): 283-299.

- Romei, V and A Smith (2022), ‘The global stagflation shock of 2022: how bad could it get?’, Financial Times, 2 May.

By: William T Gavin 05 February, 2023

This interesting post is about the short-run dynamics of inflation and other economic indicators. It ignores the longer-run effects of the $trillions transferred to local governments. businesses and consumers over the past two presidential administrations, initially spurred by the fear of Covid 19, but continued by politicians who like spenidng other people's money. This is the underlying cause of inflation in the U.S. and necesitates a Fed reaction that most likely will be needed to stay in place until the federal budget is back under reasonable control. If the inflation target is 2 percent, then the noremal level of the Fed's target rate should be 2 plus the reiskless real rate on treasury debt. The rate is closer to 3 or 4 than it is to zero.