06 February, 2017

06 February, 2017

To address the challenges that Indian corporates faced in the early 2000s in meeting their debt-servicing obligations to banks/financial institutions, RBI introduced a corporate debt restructuring programme in 2002. This column finds that in the absence of a strong legal system, this out-of-court regulatory mechanism has indeed helped Indian banks remain stable, as there has been no bank failure in India unlike in other countries.

Dealing with private-debt distress became a major policy challenge for regulators in many emerging-market economies in the last decade in the absence of a strong legal framework. In India, bankruptcy reforms were enacted for the first time in 2016 in the form of a unified ‘Insolvency and Bankruptcy Code’. In this context, World Bank estimates suggest that if banks lend one dollar in India, they can only recover 26 cents in times of distress, and it takes, on average, 4.3 years – twice as long as in China (Economist, 2015) to recover the loan. The longer the bankruptcy process takes to recover the loan the lower will be the recovery amount, when assets are divertible. Kingfisher is the most high-profile case of such bad loans where the company assets are valued significantly less today than what it would have been if the assets were sold in 2012 to recover the loans.

Corporate debt restructuring

During the early 2000s, Indian corporates faced increasing challenges in meeting their debt-servicing obligations to banks/financial institutions. High corporate-debt overhang poses a risk to banks’ balance sheets and financial stability due to increasing non-performing assets (NPAs) and corporate bankruptcies. With no unified bankruptcy code, the Reserve Bank of India (RBI) had introduced an out-of-court restructuring programme in the form of corporate debt restructuring (CDR) in 2003. The intention was to provide a speedy, cost-effective, and market-friendly alternative to in-court restructuring procedures in order to reduce risk-taking of banks faced with defaulters, and to avoid bankruptcy of viable corporates in the absence of a sound bankruptcy process. CDR system has enabled many companies to stay solvent, restructure, and finally revive, and has also helped member banks (lenders) that participated into CDR programme to reduce non-performing loans (NPLs) and stay stable. Most of the member banks, particularly public sector banks, made use of CDR mechanism and restructured a substantial portion of their distressed assets. These banks could retain the asset classification of restructured assets upon restructuring, without slipping into lower asset categories (example, sub-standard), and could even upgrade non-performing restructured assets to the standard (performing) category after a specified period and charge less to their net income for loan loss provisions1, as RBI supported this extensive regulatory forbearance on such restructured assets.

Regulatory forbearance and bank risk-taking

The implied guarantee that was provided in the form of a moratorium on loan loss provision on restructured assets has two opposing effects on bank risk. The ‘market discipline view’ argues that when banks get generous regulatory support, it diminishes investors’ incentive to monitor banking activities, which encourage more risk-taking (lower stability), amplifying the moral hazard problem. The contrary view is related to bank’s valuation arguing that generous regulatory support for banks can lower risk-taking, as perceived support inflates profitability and thereby bank valuation reducing the probability of bank failure. The question as to whether regulatory forbearance/government guarantees mitigate bank instability has been studied in the context of advanced economies, but it is still an unanswered question in the context of emerging-market economies such as India.

Assessing impact on bank stability

In the absence of any detailed analysis of the effectiveness of CDR mechanism that existed for over a decade, we assess the usefulness of such an institutional mechanism in maintaining bank stability in India2. In particular, first, we (Ahamed and Mallick 2017a) assess how the volume of restructured assets at the bank level impacted risk-taking of Indian banks over the time period 2003-2012. Establishing a causal effect in this issue is challenging: favourable regulatory support is extended to augment financial stability of banks, and it often applies to all banks; therefore, it is hard to discriminate the effects of such intervention. Our second study (Ahamed and Mallick 2017b) overcomes this challenge by exploiting variation in the membership status of banks vis-à-vis the CDR programme.

In the second study, we use a modelling strategy that is appropriate to establish causal inferences and to investigate the effectiveness of the implementation of CDR among member and non-member banks for the period 1994-2012. In this paper, we, therefore, investigate whether the banks that made use of regulatory forbearance on the restructured corporate loans could increase their stability significantly due to a concessional provisioning relished by the member banks on those assets.

Main findings

To address our research questions, we use data from the RBI and from the Centre for Monitoring the Indian Economy’s (CMIE) Prowess database. In general, our findings show that higher levels of restructured assets significantly reduced risk-taking as banks benefitted from low provisioning, and this relation is more pronounced for banks that had lower loan loss provisions. We also find that by restructuring distressed assets, public sector banks benefitted significantly more in improving their stability than private sector domestic and foreign banks (Ahamed and Mallick 2017a).

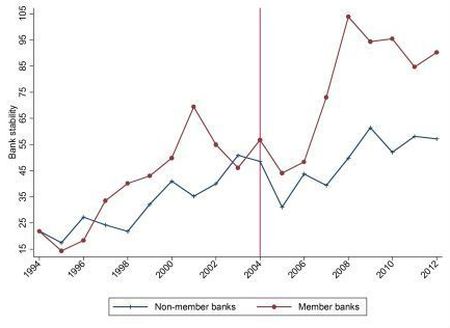

Figure 1. Evolution of banking stability, by CDR programme membership

Note: The time series of bank stability are plotted for CDR member and non-member banks. Bank stability is proxied by z-score3, which is the sum of return-on-assets and equity-asset ratio, divided by standard deviation of return-on-assets of each bank.

Note: The time series of bank stability are plotted for CDR member and non-member banks. Bank stability is proxied by z-score3, which is the sum of return-on-assets and equity-asset ratio, divided by standard deviation of return-on-assets of each bank.

In Figure 1 (Ahamed and Mallick 2017b), we separately plot the time series of z-score (a proxy measure for bank stability) for both the member and non-member banks. The stability of the member and non-member banks moved roughly together immediately before the inception of CDR mechanism. From 2005 to 2012, the stability of member banks increased substantially compared to non-member banks, as CDR was fully operational in the year 2004, and naturally, bank stability went up once they started reaping benefits of regulatory forbearance.

In addition, since market power is one of the important determinants of banking stability, we also investigate the interactive effects of CDR on stability at different levels of market power. We find that the positive effect of CDR diminishes at the higher levels of market power of the member banks. We argue that member banks with high market power possibly opted for originating risky assets under the auspices of this programme (as reflected in their risk-weighted assets). The special regulatory support on asset classification and provisioning under CDR gave more opportunities to member banks to understate NPAs and overstate net income. In April 2015, RBI effectively stopped providing regulatory forbearance on any restructured loans when the provisioning from raised to 15% from 5% in 2013, which probably explains why the size of the NPAs increased to 8.3% of total loans in June 2016, up from 4.3% by end-March 2015. The rising NPAs also suggest that CDR mechanism was beneficial for Indian banks, which kept NPAs under 4% during 2005-06 and 2013-14, but the restructuring mechanism cannot be a permanent solution.

Conclusions

Overall, it can be claimed that by reducing NPAs overhang under the guise of CDR system, RBI’s intention of having a stable banking sector has largely been achieved for the studied period. However, since 2013, the uptrend in restructuring corporate debt was worrisome due to hike in CDR provisioning norms and therefore, the regulator effectively brought the CDR system to an end in 2015 with even higher provisioning; but they should tighten the macro-prudential norms and emphasise on international best practice in asset classification and provisioning of restructured corporate loans ensuring no scope for evergreening4. With higher NPAs, banks will have to increase provisioning on existing restructured loans gradually, otherwise, any substantial losses might lead them to exhaust capital base to a point when insolvency or illiquidity would be inevitable. As other emerging-market economies are facing similar corporate distress (example, Brazilian companies), our finding implies that such type of mechanism with judicious regulatory forbearance can be an effective temporary tool for regulators in order to forestall bankruptcy of viable corporates on the one hand, and to avoid accumulating bad debt and thereby fragility of financial institutions on the other.

Notes:

- Loan loss provisioning is an expense item for banks that is allocated for risky/defaulted loans. According to provisioning norms, in respect of sub-standard assets of secured category, banks are required to keep 10%, and for the unsecured exposures, an additional 10%.

- Since we only have evidence from the creditors’ perspective (not from the debtors’ (corporates) side), we focus on stability of banks rather than firm solvency.

- Z-score can be interpreted as the number of standard deviation (SD) below the average by which returns would have to drop before all equity in the bank gets depleted. SD is a measure that is used to quantify the amount of variation or dispersion of a set of values.

- Evergreening refers to the process of banks granting new loans in the hope of partially repaying old, bad loans, instead of writing off bad loans.

Further Reading

- Ahamed, M Mostak and Sushanta Mallick (2017a), “House of restructured assets: How do they affect bank risk in an emerging market?”, Journal of International Financial Markets, Institutions and Money, Forthcoming.

- Ahamed, M Mostak and Sushanta Mallick (2017b), “Does regulatory forbearance matter for bank stability: Evidence from creditors´ perspective”, Journal of Financial Stability, 28: 163-180.

Comments will be held for moderation. Your contact information will not be made public.