20 July, 2016

20 July, 2016

Optimising the allocation of factors of production – land, capital and labour - improves productivity. In India, where evidence suggests land is severely misallocated to inefficient manufacturing firms, access to financing is disproportionately tied to access to land. This column examines the link between the misallocation of land and access to capital through financial markets. A very strong positive correlation emerges between the two, consistent with the fact that land and buildings can provide strong collateral support for accessing finance from the credit market.

A central challenge for developing countries is to promote growth by reducing the misallocation of factors of production – land, capital and labour. While there may not be such a thing as a perfectly efficient factor allocation, evidence shows that there are huge gains in growth from reducing factor misallocation. It is only optimal that efficient firms that produce more output should have access to more factors of production. In their pioneering work, Hsieh and Klenow (2009) predict a 60% increase in Indian manufacturing productivity if their measure of factor misallocation for India was brought down to US levels.

In recently completed work, we have made a number of advances looking at the misallocation of land, capital and labour (Duranton et al. 2015a). Land allocation in India is barely better than random at best, and probably worse than random. Put differently, if anything, low-productivity firms in India have better access to land and buildings than high-productivity firms. Indeed, land and buildings misallocation appears to be at the root of much of the misallocation of output and it accounts for a large share of the observed differences in labour productivity, measured as output per worker, in the manufacturing sector. More precisely, across districts, a one standard deviation1 in the misallocation of land and buildings accounts for about 20% difference in output per worker.

If land is misallocated in India, can that have repercussions on the capital allocation through financial markets? There is an important reason to believe that the two are interconnected. Most bank loans require some form of collateral to guarantee the loan. Land is simply the best form of collateral, due to its immobility (that is, the debtor can’t run off with land) and wide reusability. Land can be contrasted with a piece of specialised machinery, for example, where the borrower could seek to hide it from debt collectors or where its sale to other parties after repossession is weak. This difference is visible in terms of the amount of loan collateral possible against asset classes. While borrowers can often pledge 80% of land values against loans, for most other forms of fixed investment the loan-to-collateral value ratio is substantially lower. So, if land markets are highly distorted, then it is likely that the financial market is also distorted, given the misplaced collateral channel.

Do poorly functioning land markets distort capital markets? In another recent paper, we examine the link between the misallocation of land inputs and growing evidence on credit constraints using plant-level data on the organised and unorganised sectors in India (Duranton et al. 2015b). The focus of the analysis was the hypothesis that land misallocation might be an important determinant of financial misallocation, due to the role of land as collateral against loans. Using district-industry variations, the analysis finds evidence to support this hypothesis, although it does not find a total reduction in the intensity of financial loans or those being given to new entrants.

Financial misallocation

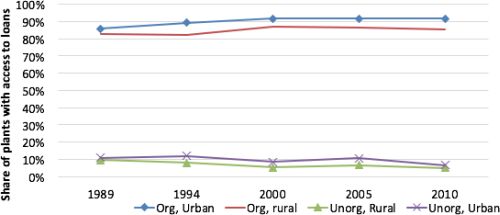

There are many interesting trends to observe in the data, given in Figure 1. First, firms in the organised sector have much higher access to bank loans compared to firms in the unorganised sector. Second, irrespective of the urban/rural location, the share of plants accessing external loans in the organised sector has increased over time. In contrast, it has declined for the unorganised sector. Third, there are urban-rural disparities in access to finance, with rural locations lagging behind their urban counterparts. However, the share of urban plants in the organised sector has declined, while that in the unorganised sector has increased. That the organised sector is de-urbanising and the unorganised sector is urbanising is a trend we have observed in earlier work on India’s spatial development (Ghani et al. 2012).

Figure 1. Access to loans in organised and unorganised sectors, by region

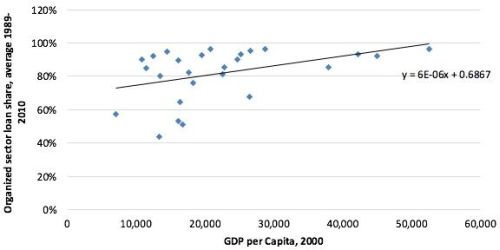

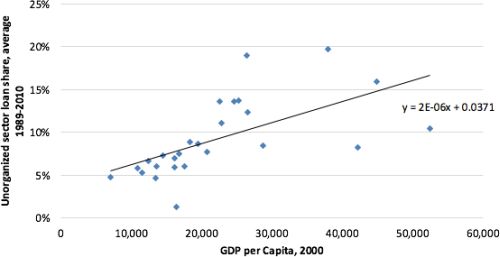

There are also huge spatial disparities in access to finance within India. Access is significantly higher in the leading regions compared to lagging regions. Leading states like Maharashtra show important depth of financing for firms. At the other extreme are states like Bihar where access to loans is very low. More specifically, plotting the share of plants with access to loans against Gross Domestic Product (GDP) per capita (Figure 2), we note that richer states are strongly associated with higher access shares. This is true for both the organised (Figure 2a) and the unorganised (Figure 2b) sectors. States like Gujarat, Punjab, Haryana and Rajasthan that have higher per capita income have access to financial loans for over 95% of the organised sector plants. On the other hand, lagging states like Bihar and Manipur perform poorly in providing external credit support for both the organised and unorganised sectors.

Figure 2. Access to loans and GDP per capita

Organised sector

Unorganised sector

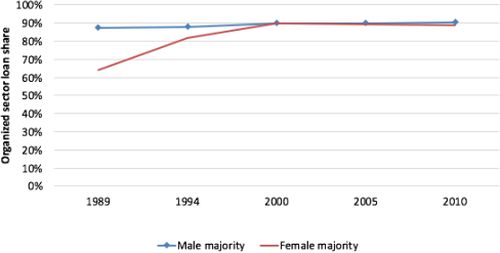

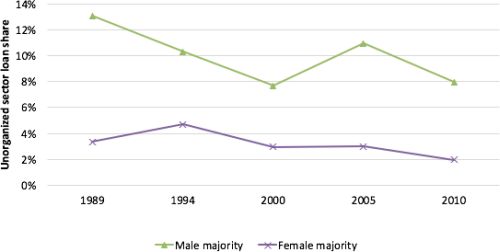

There is also significant disparity against women-owned enterprises in India. Although the gap between the access shares of female employee-dominated plants vis-à-vis male employee-dominated plants is closing in the organised sector, this gap is not shrinking in the unorganised sector. The same is true for female-owned plants in the unorganised sector. Figure 3 makes this point by using the share of males versus female employees split, and plotting the access share to loans for plants with primarily male employees and primarily female employees for the organised (Figure 3a) and the unorganised (Figure 3b) sectors.

Figure 3. Access to loans, using employee split between male and female majority

Organised sector

Unorganised sector

Misallocation and productivity

Past studies have shown that growth can be enhanced by the reallocation of the factors of production from a less-productive to a more-productive firm. Thus, the ranking of firms by factor usage should reflect their relative productivity ranking and hence be perfectly correlated under optimum allocation. Conversely, a less-than-perfect correlation between productivity and factor usage indicates a misallocation of factors across firms. The lower this correlation between productivity and factor usage, the greater is the extent of misallocation of factors of production.

We develop indices of misallocation for output, value added, and factors of production (Duranton et al. 2015a). Following this approach, our companion paper (Duranton et al. 2015b) computes indices for measuring misallocation in financial markets. These measures of misallocation are then used in various district-industry-level regressions that examine both the determinants and the implications of misallocation, especially how the misallocation in access to finance is linked to the misallocations in land, buildings and labour.

Our work suggests that there is a very strong positive correlation of land and building misallocation with that of financial access. This is consistent with the fact that land and buildings can provide strong collateral support for accessing finance from the credit market2.

Labour market misallocations serve as an important contrast to land and building misallocation, with the former showing an inconsistent relationship with financial loan misallocation. Although our results do not provide a final answer to the causal connections, they do provide substantial confirmation in the links between land misallocation and financial misallocation.

Conclusions

These emerging trends in factor misallocation are worthy of more attention. The unorganised sector accounts for nearly 80% of employment and about half of the value of land and buildings held in the manufacturing sector in India. Yet, the value of financial loans reported in this sector is barely 2-6% of the value of total loans reported in the manufacturing sector. One question that is worth asking is whether misallocation in land and buildings in the unorganised sector acutely accentuates the misallocation in access to finance.

Another related question is whether the distortion in land markets sharply hits women entrepreneurs, who have historically had much lower access to land, by way of laws that were much against inheritance of land. In the presence of land market distortions, can women-owned enterprises take advantage of other forms of collateral, like plants and machinery? Can financial liberalisation policies help break the strong link between distortions in land and loan markets? We hope to address some of these issues in our future endeavours.

This column first appeared on VoxEU.

Notes:

- The standard deviation is a statistical measure of the variation or dispersion in a distribution.

- This result remains robust to considering alternative specifications with additional controls, to using misallocation from the combined organised and unorganised sector and to alternative indices for measuring access to financial markets.

Further Reading

- Duranton, G, E Ghani, AG Goswami and W Kerr (2015a), ‘The misallocation of land and other factors of production in India’, World Bank Working Paper No. 7221.

- Duranton, G, E Ghani, AG Goswami and W Kerr (2015b), ‘Effects of Land Misallocation on Capital Allocations in India’, World Bank Working Paper No. 7451.

- Ghani, E, AG Goswami and WR Kerr (2012), ‘Is India´s manufacturing sector moving away from cities?’, NBER Working Paper No. 17992.

- Hsieh, Chang-Tai and Peter J Klenow (2009), “Misallocation and manufacturing TFP in China and India”, Quarterly Journal of Economics, 124(4):1403-1448. Available at: http://faculty.chicagobooth.edu/chang-tai.hsieh/research/mmtfp.pdf

Comments will be held for moderation. Your contact information will not be made public.